How Insurance Appraisal Has Become the Insurance Industry’s Most Effective Accountability Shield

Has Insurance Appraisal Outlived Its Original Purpose?

Insurance appraisal was originally designed to resolve simple disagreements about the value of a covered loss. Today, many policyholders and industry professionals are asking a different question: Has appraisal evolved into an accountability shield that benefits insurers more than the consumers it was intended to protect?

Insurance appraisal is a contractual dispute resolution mechanism built directly into most commercial and multifamily property insurance policies — and it may be the most consequential clause your team has never fully read. Before answering the issues revolving around the ambiguity and abuse of insurance appraisals, one must ask themselves, if appraisal is truly intended to protect policyholders, why are so many insurers eager to include it in their policy and invoke it?

Quick Answer: What Is Insurance Appraisal?

| Question | Answer |

|---|---|

| What is it? | A binding alternative dispute resolution process for resolving disagreements over the dollar amount of a covered loss |

| Who uses it? | Either the policyholder or the insurer can invoke it |

| What does it decide? | The amount of loss only — not whether coverage applies |

| Who is involved? | Two party-appointed appraisers + one neutral umpire |

| Is the result binding? | Yes — in most, not all cases, with very limited grounds for appeal |

| How fast? | Appraisal is often marketed as a 30–90 day process, but large commercial claims frequently take several months or longer due to appraiser selection, umpire disputes, expert investigations, scheduling conflicts, procedural disagreements, and post-award coverage disputes. While appraisal may resolve valuation issues faster than litigation, it does not necessarily resolve the underlying claim. |

| Who pays? | Each party pays their own appraiser; umpire costs are split equally |

Is Appraisal Cheaper Than Hiring a Public Adjuster or Attorney?

Not necessarily.

One of the most common arguments in favor of appraisal is that it is less expensive than hiring a public adjuster or pursuing litigation. While appraisal may appear less expensive at first glance, the comparison is often misleading because the costs, risks, and outcomes are fundamentally different.

A public adjuster is typically involved from the beginning of the claim and works to identify damages, document losses, prepare estimates, negotiate with the insurance company, and maximize the overall settlement. In contrast, appraisal is generally invoked only after a dispute has already developed.

Likewise, attorneys are typically retained to resolve coverage disputes, bad-faith conduct, statutory violations, or other legal issues that appraisal panels have no authority to decide.

Perhaps more importantly, appraisal is not free. Policyholders are generally required to:

-

Pay their own appraiser.

-

Share the cost of the umpire.

-

Retain engineers, consultants, contractors, or other experts when necessary.

-

Invest significant time and resources preparing their position.

In large commercial claims, these expenses can quickly reach thousands or even tens of thousands of dollars.

The better question is not whether appraisal is cheaper.

The better question is whether appraisal produces a better outcome.

A process that costs less but results in an incomplete investigation, an undervalued claim, unresolved coverage disputes, or a loss of legal leverage may ultimately be far more expensive than obtaining qualified professional representation at the outset.

For many policyholders, the most cost-effective strategy is not appraisal at all—it is properly documenting the claim, retaining qualified experts when necessary, and presenting a well-supported claim before a valuation dispute ever reaches the appraisal stage.

The cheapest process is not necessarily the least expensive outcome.

“It’s faster.”

Maybe. But faster than what? And does it actually solve the problem

How Fast Is Appraisal Really?

The insurance industry frequently promotes appraisal as a faster alternative to litigation, often suggesting disputes can be resolved within 30 to 90 days. In reality, that timeline is often the exception rather than the rule in large commercial and multifamily claims.

Before the appraisal panel can even begin evaluating damages, the parties must select appraisers, agree on an umpire, exchange documentation, review engineering reports, inspect the property, and resolve procedural disputes. If the appraisers cannot agree on an umpire, court intervention may be required, adding additional delay.

Even after an appraisal award is issued, the claim may not be over. Coverage disputes, payment disagreements, policy limitations, depreciation calculations, deductibles, and other issues can remain unresolved.

The more important question is not whether appraisal is faster than litigation.

The more important question is whether appraisal produces a complete and final resolution of the claim.

For many policyholders, the answer is no.

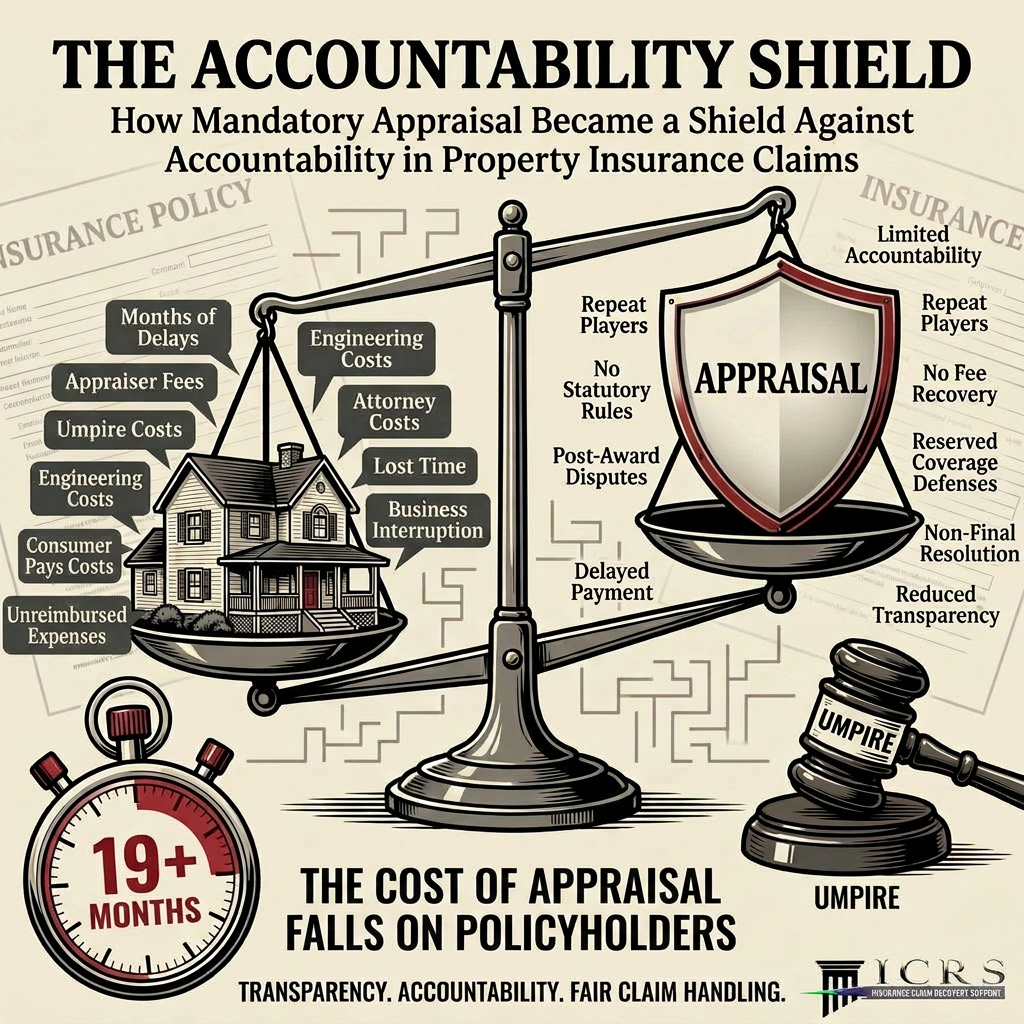

While appraisal is often described as a simple way to resolve valuation disputes, many policyholders are surprised to learn that the process can cost thousands of dollars, lacks meaningful regulatory oversight, allows unlicensed participants to determine the value of major losses, and may still leave coverage disputes unresolved even after a binding award is issued.

Appraisal may have a limited role in relatively small valuation disputes where coverage has been accepted and the only disagreement is pricing.

Here is the uncomfortable reality for commercial property owners, apartment operators, HOAs, and institutional building managers: when a major storm, fire, or hail event hits, the number your insurer puts on paper and the number it actually costs to make your property whole are rarely the same.

In hail and storm damage claims alone, valuation gaps between insurer estimates and policyholder estimates average 20–40%. On a $2 million commercial claim, that gap can mean $400,000 to $800,000 in disputed dollars — and the difference between a full recovery and a financially crippling shortfall.

That’s exactly the scenario the appraisal clause appears to be designed to resolve. ⚖️

But here’s what most policyholders don’t know: the appraisal process has increasingly become something else entirely. Carriers have learned to use it strategically — as a procedural shield that can limit bad faith exposure, reset timelines, and quietly shift leverage away from the policyholder before the first appraiser is even appointed.

Understanding how appraisal actually works — and how it can be used against you if you’re not prepared — is no longer optional for commercial property owners managing real risk.

I’m Scott Friedson, CEO of Insurance Claim Recovery Support (ICRS) and a multi-state licensed public adjuster with over 15 years of experience and more than $250 million in large-loss insurance appraisal and claim settlements on behalf of commercial and multifamily property owners. In the sections below, I’ll walk you through exactly how this process works, where it breaks down, and what accountability in a fair appraisal actually looks like.

The Mechanics of the Insurance Appraisal Process in Commercial Claims

To understand how the insurance appraisal process operates, we first have to look at the contract itself. Commercial and multifamily property policies (such as the ISO CP 00 10 form or customized manuscript policies) contain highly customized, carrier-specific variations that dictate how, when, and under what rules an appraisal can be conducted.

When a major loss occurs — whether it’s a catastrophic fire at an industrial facility or hurricane-force winds ripping through an apartment complex — the policyholder must first Assess the Damages and submit a detailed proof of loss. If a profound disagreement on the valuation occurs, either party can formally invoke the appraisal clause. To navigate this successfully, policyholders should consult a comprehensive Property Damage Claims Complete Guide to ensure they do not inadvertently waive their rights.

Once the appraisal clause is formally invoked in writing, the mechanics of the process unfold through a series of highly structured steps:

-

- Appointment of Appraisers: Each party must select a competent and independent appraiser within a specified timeframe (typically 20 days). These appraisers act as the designated valuation representatives for their respective sides.

- Selection of the Umpire: The two appointed appraisers are tasked with jointly selecting a qualified, neutral umpire. If they cannot agree on an umpire, they must petition a local court of competent jurisdiction to appoint one.

- Assessment and Negotiation: Both appraisers independently evaluate the property damage, reviewing estimates, engineering reports, and restoration bids. They then meet to compare their findings and attempt to reach an agreement on the dollar value of the loss.

- The Binding Award: If the two appraisers agree on the value, they sign off on the award, and the dispute is resolved. If they disagree, they submit their differing positions to the neutral umpire. Any agreement reached and signed by any two of the three members of the appraisal panel (e.g., one appraiser and the umpire) constitutes a binding award. This is known as a “2-of-3 agreement.”

-

The “Binding” Award—But Not Necessarily the Final Word

Once the appraisal process is complete, the members of the appraisal panel attempt to reach an agreement on the amount of the loss. If both appraisers agree on the value of the claim, they sign an appraisal award, and that amount becomes binding on the parties. If the appraisers cannot agree, their respective positions are submitted to the neutral umpire for consideration.

Under most appraisal provisions, an agreement signed by any two members of the three-person appraisal panel constitutes a valid and binding appraisal award. This is commonly referred to as a “2-of-3 agreement.” For example, if one appraiser and the umpire agree on the amount of the loss, their signed award is sufficient to establish the appraisal value, even if the other appraiser disagrees.

However, policyholders should understand that a “binding” appraisal award is often less binding than it appears.

Many insurance policies contain language stating that participation in appraisal does not waive the insurer’s rights under the policy. In other words, while appraisal may determine the amount of loss, the insurer frequently reserves the right to deny all or part of the claim based on coverage defenses, policy exclusions, deductibles, limitations, conditions, or other legal arguments.

As a result, a policyholder may spend significant time and money obtaining an appraisal award, only to discover that the insurer contends some or all of the awarded damages are not covered under the policy. In some cases, the carrier may pay only a portion of the award or continue disputing specific components of the claim despite the appraisal outcome.

This distinction is critical. Appraisal generally determines the value of the loss, but it does not necessarily determine whether the insurer must pay that amount. Consequently, policyholders should carefully evaluate any unresolved coverage issues before agreeing to appraisal, as a favorable award does not always guarantee a favorable payment.

Appraisal Often Favors the Party with Greater Resources

One of the most overlooked problems with appraisal is the inherent imbalance of resources between insurance companies and policyholders.

Insurance carriers routinely retain engineers, consultants, attorneys, and other experts whose opinions can significantly influence the outcome of a claim. By contrast, many property owners lack the financial resources necessary to hire their own experts to challenge those opinions. As I discussed during a recent industry panel on appraisal and litigation avoidance, policyholders should be permitted to bring their own engineers and experts into the process because they often do not have the insurance company’s money to fight expert opinions that may ultimately drive claim decisions.

This observation highlights a fundamental flaw in the appraisal system. The process is often portrayed as a neutral method of resolving disputes, yet the parties frequently enter the proceeding with vastly different financial resources and access to expertise. The result is a system in which the side with greater resources may enjoy a significant advantage before the appraisal even begins.

The concern becomes even more troubling when insurers rely on expert opinions to justify claim decisions and then point to those opinions as evidence that their conduct was reasonable. In such situations, appraisal can become less about independently evaluating the loss and more about determining which side can assemble the most persuasive team of experts.

A truly fair dispute-resolution process should not depend on which party has the larger budget. Until meaningful reforms are implemented, policyholders should recognize that appraisal is not always the level playing field it is often portrayed to be.

To see how this process stacks up against other legal and quasi-judicial resolution routes, we can compare them directly:

| Feature | Insurance Appraisal | Arbitration | Litigation (Lawsuit) |

|---|---|---|---|

| Scope of Dispute | Strictly limited to the dollar “amount of loss” | Broad disputes including coverage and policy interpretation | Full resolution of all legal, coverage, and damage disputes |

| Who Decides? | Two independent appraisers and a neutral umpire | One or more professional arbitrators | A judge and/or a jury |

| Rules of Evidence | Informal; no depositions, court reporters, or strict rules | Semi-formal; defined by arbitration agreements | Strict adherence to state or federal rules of civil procedure |

| Average Timeline | 30 to 90 days | 6 to 12 months | 12 to 24+ months |

| Average Cost | Varies significantly; often several thousand dollars to tens of thousands of dollars in large commercial claims. Each side pays their own appraiser plus split umpire fees) | High (Arbitrator fees, legal representation, filing costs) | Very High (Attorney fees, expert witnesses, court costs) |

| Enforceability | Binding; extremely difficult to challenge in court | Binding; limited avenues of appeal | Binding; subject to standard appellate court review |

Watch: My Perspective on Fair Appraisal and Litigation Avoidance

In the video below, I discuss why policyholders should be permitted to bring engineers and experts into the appraisal process and why resource disparities can create an uneven playing field.

In this discussion on policyholder rights, I explain why policyholders should have access to qualified engineers and experts during appraisal proceedings and why resource disparities between insurers and policyholders can create an uneven playing field. The issue is not whether experts should be involved—the issue is whether both sides have a fair opportunity to present them.

The Resource Imbalance Problem

Throughout my career representing policyholders, I have consistently observed one of the most significant flaws in the appraisal process: the unequal resources available to the parties involved.

Insurance companies often have access to teams of engineers, consultants, attorneys, and other experts whose opinions can shape the outcome of a claim. Property owners, on the other hand, are frequently forced to make critical decisions without the same financial resources or access to specialized expertise.

As I discussed during a recent industry panel on appraisal and litigation avoidance, policyholders should have the ability to present engineers and other qualified experts when necessary because many simply do not have the insurance company’s budget to challenge opinions that may ultimately drive claim decisions. When one side has substantially greater resources, the process can become less about determining the true amount of loss and more about which party can assemble the most persuasive team of professionals.

This raises an important question: Is appraisal truly a level playing field?

For many policyholders, the answer is no. The reality is that appraisal often begins with a structural imbalance that favors sophisticated insurance carriers that participate in these proceedings every day, while most policyholders encounter the process only once in their lifetime.

A fair dispute-resolution system should focus on the facts, policy language, and actual damages—not on which party has the greater financial resources. Until meaningful reforms are implemented, policyholders should carefully consider whether appraisal is the most effective path for resolving a claim dispute.

Appraisal May Be Worth Considering When:

- The insurance company has accepted coverage for the loss.

- The scope of damage has been fully identified and documented.

- There are no significant unresolved causation or coverage disputes.

- The only remaining disagreement involves the cost to repair or replace the damaged property.

- The anticipated benefit of appraisal outweighs the costs of hiring an appraiser and sharing umpire expenses.

For example, if both parties agree that a commercial roof must be replaced and the only disagreement is whether the replacement cost is $185,000 or $225,000, appraisal may provide a mechanism for resolving that limited valuation dispute. These relatively small pricing disagreements are arguably the situations for which appraisal was originally designed. By contrast, using appraisal to resolve six-figure or seven-figure disputes involving competing engineering opinions, scope disagreements, and complex coverage issues often stretches the process far beyond its intended purpose.

Appraisal Should Generally Be Avoided When:

- The insurer is disputing coverage.

- The cause of loss remains contested.

- The full extent of the damage has not been determined.

- Engineers, contractors, or other experts are still evaluating the property.

- Significant damages have not yet been presented to the insurer.

- The dispute involves claim handling issues, unreasonable delays, or allegations of bad faith.

- The insurer is attempting to use appraisal as a substitute for a complete and thorough investigation.

In these situations, appraisal can actually work against the policyholder by narrowing the dispute to pricing issues while leaving critical questions regarding coverage, causation, and claim handling unresolved.

Our Position

If appraisal serves any legitimate purpose within the property insurance claims process, it should be limited to relatively small valuation disputes where coverage has been accepted and both parties simply disagree on the reasonable cost of repairs. Unfortunately, appraisal is increasingly being used to resolve large, complex disputes involving substantial amounts of money and issues that extend well beyond valuation.

Before invoking appraisal, policyholders should fully understand the costs, limitations, and potential consequences of the process. In many cases, appraisal should be viewed as a last resort rather than a preferred method of claim resolution.

When handling these high-exposure events, engaging in Large Loss Claims Handling and seeking expert Large Loss Claims Consulting is critical.

The Scope of Appraisal: Amount of Loss vs. Coverage and Causation

One of the most heavily contested battlegrounds in commercial property insurance is the dividing line between coverage and valuation.

-

- Coverage Issues: These involve policy interpretation. Did the damage occur during the policy period? Is the specific peril (e.g., flood vs. windstorm) covered? Does an exclusion apply? These are legal questions that cannot be decided by an appraisal panel.

-

- Valuation Issues: These involve the physical scope and cost of repairs. What is the actual cash value (ACV) or replacement cost value (RCV) of the damaged property? What is the cost of the materials and labor required to return the building to its pre-loss condition? These are factual questions that are the exclusive domain of the appraisal panel.

The “gray zone” occurs when causation is mixed. For example, if a commercial roof has pre-existing wear and tear but is subsequently hit by a severe windstorm, the carrier may argue that only a small portion of the roof damage was caused by the storm (a causation/coverage defense), while the policyholder argues the entire roof must be replaced.

In states like Texas, courts have ruled that appraisal panels can determine causation when assessing the amount of loss, as causation is often inextricably linked to the scope of damage. Under the Texas Insurance Code, including Texas Statutes Chapter 541 (unfair claim settlement practices) and Chapter 542 (Prompt Payment of Claims Act), carriers cannot use a pending appraisal to indefinitely delay their statutory payment obligations.

Meanwhile, in Florida, litigation costs have historically soared because carriers frequently try to resolve coverage questions in court before allowing an appraisal to proceed. When these complex coverage and causation issues intersect, having a sophisticated strategy for Insurance Settlement Negotiation is paramount to ensure your claim does not get trapped in endless legal limbo.

Systemic Insurer Tactics and the “Cost of Doing Business” Model

In a perfect world, insurance companies would quickly and fairly adjust claims, paying exactly what is owed to restore damaged commercial and multifamily properties. In the real world of corporate risk management, however, major carriers operate under a “cost of doing business” model. Under this model, systematically underpaying claims, delaying settlements, and forcing commercial policyholders into expensive dispute resolution processes is viewed as a highly profitable financial strategy.

This systemic scrutiny is not just an industry rumor; it is a matter of public record and regulatory action. For instance, in April 2026, a major carrier’s aggressive claim practices culminated in a State Farm $15.6M settlement following allegations of bad faith and systematic underpayment of storm-related commercial property damage claims.

Further west, California regulators have taken massive steps to address systemic carrier misconduct. An extensive NYT California article detailed how commercial and multifamily property owners were left stranded after catastrophic wildfires. This led to a formal California Enforcement Action targeting the carrier’s handling of these claims.

The scope of these violations was widely reported by major media outlets, with The Guardian highlighting the carrier’s failure to properly investigate wildfire losses on commercial and multifamily assets, and CNN reporting on how commercial policyholders were systematically underpaid for smoke, ash, and thermal damage.

These regulatory actions expose a broader pattern: carriers frequently rely on adjuster licensing gaps, deploying out-of-state catastrophe adjusters who lack the licensing or local knowledge required to accurately assess commercial property damage. Furthermore, carriers often ignore critical environmental protocols, disregarding “dry log” records and failing to account for the specialized restoration techniques required to safely remediate large-scale commercial structures.

How Carriers Weaponize the Insurance Appraisal to Avoid Bad Faith Litigation

For a commercial policyholder, bad faith statutes (such as Texas Insurance Code Chapters 541 and 542) are the ultimate hammer. They allow policyholders to recover statutory interest penalties, attorney fees, and treble damages if an insurer unreasonably delays or denies a claim.

To escape this liability, carriers have learned to weaponize the insurance appraisal clause as an accountability shield.

Here is how the tactic works:

-

- The carrier severely underpays a claim, offering a fraction of its true value.

-

- The policyholder threatens a bad faith lawsuit.

-

- The carrier immediately demands appraisal.

-

- Because the appraisal process is contractual and binding, courts in many jurisdictions will stay (pause) any pending bad faith litigation while the appraisal is underway.

-

- Once the appraisal panel issues a binding award—which is often significantly higher than the carrier’s original offer—the carrier pays the award within the policy’s standard payment window.

-

- The carrier then argues that because they paid the appraisal award timely, they cannot be held liable for bad faith or statutory interest penalties, effectively wiping out the policyholder’s legal leverage.

Furthermore, in states like Texas, the statute of limitations continues to run even while an appraisal is pending. This means that if a policyholder is not careful, they can easily run out of time to file a protective lawsuit in time-sensitive cases. This is why commercial property owners in major Texas metropolitan hubs—including Austin, Dallas, Fort Worth, Houston, San Antonio, Lubbock, San Angelo, Waco, Round Rock, Georgetown, and Lakeway—must be incredibly strategic. Knowing How to Negotiate a Settlement with an Insurance Claims Adjuster is essential to avoid falling into these sophisticated carrier traps.

Does Appraisal Encourage Poor Claim Handling?

One of the least discussed consequences of the appraisal process is the incentive structure it creates for insurance companies and their adjusters.

In virtually every other profession, individuals are expected to perform their jobs correctly the first time. Contractors are expected to properly scope repairs. Engineers are expected to accurately assess structural conditions. Accountants are expected to correctly prepare financial records. When mistakes occur, there are often consequences.

Yet appraisal can create a system where insurance adjusters face reduced pressure to fully investigate, properly scope, and accurately value a loss from the outset.

Why?

Because appraisal is always waiting in the background.

If an adjuster overlooks damages, undervalues repairs, ignores expert recommendations, or submits an estimate that fails to reflect the true cost of restoration, the carrier can often argue that any disagreement can simply be resolved later through appraisal.

This creates a troubling question:

If appraisal exists as a fallback mechanism, what incentive does an insurer have to get the claim right the first time?

In many cases, the answer may be “less than they otherwise would.”

The problem becomes even more pronounced when appraisal is used after months of delay, incomplete investigations, or significant underpayments. Instead of focusing on whether the claim was properly adjusted, the discussion shifts toward valuation. The original claim handling deficiencies become secondary, and the policyholder is often required to spend additional time and money participating in appraisal to obtain the benefits they should have received through a proper adjustment process in the first place.

No other consumer protection system would tolerate this approach.

Imagine a contractor intentionally underbidding a project with the expectation that disputes will be resolved later. Imagine a tax preparer knowingly filing inaccurate returns because corrections can be made during an audit. Most consumers would view that conduct as unacceptable.

Insurance claims should be no different.

A dispute-resolution process should not create incentives for poor performance. If anything, the existence of appraisal may reduce the urgency for carriers to conduct thorough investigations and arrive at accurate claim valuations before a dispute arises.

At a minimum, policymakers should examine whether appraisal is functioning as a legitimate valuation tool—or whether it has inadvertently become a safety net that allows inadequate claim handling to persist without meaningful consequences.

Appraisal May Create a Moral Hazard

In economics and public policy, a “moral hazard” occurs when individuals or organizations take greater risks because they do not bear the full consequences of their actions.

The existence of appraisal may create a similar problem in the insurance claims process.

If adjusters know that significant valuation disputes can ultimately be shifted into appraisal, the incentive to thoroughly investigate, properly scope, and accurately value a claim during the initial adjustment process may be reduced. Instead of ensuring the claim is handled correctly from the outset, there may be an expectation that unresolved issues can simply be sorted out later through appraisal.

Consumer protection laws were enacted to encourage prompt, fair, and accurate claim handling. Any dispute-resolution process that weakens those incentives deserves careful scrutiny from regulators and lawmakers.

If Consumer Protection Laws Already Exist, Why Do We Need Appraisal?

State legislatures have spent decades creating laws designed to protect policyholders from unfair insurance claim practices.

In Texas alone, policyholders benefit from:

- Texas Insurance Code Chapter 541 (Unfair Claim Settlement Practices)

- Texas Insurance Code Chapter 542 (Prompt Payment of Claims Act)

- Common-law bad faith remedies

- Statutory interest penalties

- Attorney fee recovery in certain circumstances

- Regulatory oversight by the Texas Department of Insurance

These laws exist for a reason. Legislators recognized that insurance companies possess significantly greater financial resources, expertise, and bargaining power than most policyholders. Consumer protection statutes were specifically designed to discourage claim delays, underpayments, inadequate investigations, and other unfair claim practices.

This raises an important question:

If these protections already exist, why should policyholders voluntarily move their dispute into an appraisal process that has no discovery, no meaningful regulatory oversight, limited transparency, limited appeal rights, and no mechanism for determining whether the insurer acted reasonably during the adjustment process?

More importantly, why would an insurance company be eager to invoke appraisal if the claim could otherwise be evaluated under statutes designed to punish unreasonable claim handling?

The answer may explain much of appraisal’s growing popularity among insurers.

Unlike bad-faith litigation, appraisal focuses almost exclusively on the amount of loss. It generally does not determine whether the insurer conducted a proper investigation, acted reasonably, complied with prompt-payment requirements, or engaged in unfair claim settlement practices. As a result, appraisal can redirect the dispute away from questions of accountability and toward a narrow valuation exercise.

To be clear, appraisal may have a legitimate role in resolving small valuation disagreements where coverage has been accepted and both sides simply disagree on price. But when appraisal is used to resolve disputes involving significant underpayments, claim delays, inadequate investigations, or potential bad-faith conduct, policyholders should carefully consider whether they are exchanging statutory protections for a process that offers significantly fewer consumer safeguards.

The better question is whether appraisal improves consumer protection—or simply replaces it.

The process itself begs to question why a system with fewer consumer protections is being promoted as the preferred alternative to one that already has them.

The Licensing Double Standard

Insurance carriers frequently argue that strict licensing requirements are necessary to protect consumers from unqualified individuals assisting with insurance claims. Contractors are accused of unauthorized public adjusting, aka UPPA. Public adjusters must obtain licenses, complete continuing education, comply with ethical requirements, and remain subject to regulatory oversight.

Yet in many appraisal proceedings, individuals who are not licensed adjusters, engineers, architects, attorneys, or contractors are permitted to participate in determining the value of losses worth hundreds of thousands or even millions of dollars.

If consumer protection is truly the goal, why does the industry tolerate a system in which some of the most consequential decisions in a property insurance claim can be made by individuals operating with little regulatory oversight, no centralized reporting requirements, and limited accountability?

The inconsistency is difficult to ignore and further illustrates why the appraisal process deserves closer scrutiny from regulators and lawmakers.

No Regulatory Visibility

Texas tracks:

- Licensed public adjusters

- Insurance agents

- Carriers

- Complaints

- Enforcement actions

Yet there is virtually no public reporting on:

- How often appraisal is invoked

- Who invokes it

- Award amounts

- Post-award payments

- Repeat appraisers

- Repeat umpires

- Consumer complaints against appraisers

The State of Texas has more visibility into licensed public adjusters than it does into the appraisal process itself.

Where Is the Data?

Despite the significant financial impact appraisal can have on policyholders, there is no centralized database tracking appraisal outcomes, repeat appraisers, repeat umpires, award amounts, post-award payments, consumer complaints, or disciplinary actions. Policymakers are effectively being asked to trust a dispute-resolution system that operates largely in the shadows. Before appraisal is expanded or further protected by law, regulators should first require transparency regarding how the system actually performs.

Follow the Money

Every participant in the appraisal process is paid because appraisal exists.

Appraisers are paid.

Umpires are paid.

Consultants are paid.

Experts are paid.

Attorneys are often paid.

The only party paying these additional costs is usually the policyholder, either directly or indirectly.

Before appraisal is invoked, policyholders should ask a simple question: Who benefits financially from expanding the appraisal process, and who bears the risk if the process fails to deliver a fair outcome?

Does the Appraisal Process Create Incentives for Everyone to Escalate Disputes?

Insurance companies are not the only parties that can benefit from appraisal.

In some situations, contractors, consultants, attorneys, appraisers, engineers, and other claim participants may also have financial incentives that align with moving a dispute into appraisal rather than resolving it during the normal adjustment process.

For example, a contractor may genuinely believe the carrier’s estimate is inadequate and that appraisal will produce a more accurate valuation. Likewise, attorneys, consultants, appraisers, engineers, and other claim professionals may recommend appraisal because they believe it will improve the outcome. However, policymakers should recognize that nearly every participant in the appraisal process has a financial interest in the process itself continuing.

This does not mean these parties are acting improperly. In many cases, appraisal may be pursued in good faith and with the genuine belief that it will produce a fair result.

However, policymakers should recognize a simple reality:

Virtually every participant in the appraisal process is paid because appraisal occurs.

The policyholder is often the only participant who is not guaranteed a financial benefit from the process itself.

That is why policyholders should carefully evaluate recommendations to invoke appraisal—regardless of whether the recommendation comes from an insurance company, contractor, consultant, attorney, or appraiser.

The relevant question is not:

“Who wants appraisal?”

The relevant question is:

“Does appraisal genuinely serve the policyholder’s interests in this specific claim?“

Environmental Hazards and Technical Gaps in Carrier Appraisals

When a commercial building or multifamily complex suffers a major loss, the damage is rarely skin-deep. Yet, carrier-appointed appraisers routinely overlook complex environmental hazards and technical restoration protocols to keep their repair estimates artificially low.

Consider what a comprehensive commercial restoration requires:

-

- OSHA Standards: Commercial job sites must comply with strict federal safety guidelines, which dramatically impact labor costs, containment setups, and project timelines.

-

- Industrial Hygienists: After a fire or water loss, independent industrial hygienists must be brought in to test for toxic soot, particulate matter, and chemical residues.

-

- Mold and Asbestos Protocols: Older commercial properties and multifamily units frequently contain hidden asbestos or require specialized mold remediation. These require strict containment, negative air pressure machines, and certified hazardous material disposal.

-

- Dry Log Records: Following a water intrusion event, commercial restoration contractors must maintain detailed daily moisture readings (dry logs) to prove the structure has been fully dried. Carriers often ignore these logs, writing estimates that assume basic structural drying without replacing damaged, contaminated drywall and insulation.

When carrier appraisals ignore these critical technical requirements, they leave multifamily operators and HOAs exposed to massive post-claim liabilities, including structural rot, poor indoor air quality, and potential lawsuits from tenants or residents.

The question is not whether appraisers are qualified to estimate construction costs. Many are.

The question is whether a three-person appraisal panel is the appropriate forum for evaluating complex industrial hygiene issues, OSHA compliance requirements, environmental remediation protocols, hazardous material handling, engineering causation opinions, and life-safety concerns that often arise in large commercial losses.

These disputes frequently extend far beyond simple questions of valuation and highlight how far modern appraisal has drifted from its original purpose.

Fact vs. Myth: Navigating the Appraisal Process

Navigating an appraisal is a legal and financial minefield. To protect your commercial investment, you must be able to separate industry myths from contractual realities.

Myth #1: Anyone can serve as your appraiser, including your contractor or your active public adjuster.

-

- Fact: Most commercial policies require appraisers to be “competent and disinterested” or “impartial.”

-

- Translation Callout: If you appoint an appraiser who has a direct financial interest in the outcome of your claim—such as a public adjuster working on a contingency fee or a contractor who has already signed a construction contract for the repairs—the carrier will immediately challenge their qualifications in court. In Florida, for example, there is a prominent 3-1 appellate district split on whether a public adjuster with a contingency fee agreement can legally serve as a disinterested appraiser. To avoid having your appraisal thrown out, you must hire a qualified, independent third-party appraiser.

Myth #2: The umpire’s job is to split the difference between the two appraisers’ estimates.

-

- Fact: A qualified umpire does not simply add the two estimates together and divide by two.

-

- Translation Callout: The umpire’s role is to act as an objective judge. They review the detailed evidence, line-item estimates, and engineering reports submitted by both sides, and make an independent determination of the true cost of repairs. A skilled appraiser representing the policyholder must present a bulletproof, evidence-backed case to ensure the umpire understands the full scope of the commercial loss.

To ensure you are fully prepared before entering this process, review The Case for Engaging Public Adjusters Early in Large Loss Claims and understand how Public Adjuster Fees for Property Damage Claims are structured to protect your recovery.

Frequently Asked Questions About Commercial Property Appraisals

Does Invoking Appraisal Waive Bad Faith Claims?

Not necessarily. Depending on the jurisdiction, policy language, and timing of the claim, policyholders may still retain statutory and common-law remedies for bad-faith conduct. However, appraisal can significantly alter litigation strategy and may reduce leverage if not carefully managed. Policyholders should consult qualified legal counsel before invoking appraisal in any claim involving delay, underpayment, or potential bad-faith conduct.

Can an appraisal award be challenged or overturned?

In 95%+ of cases, an appraisal award is completely binding and cannot be overturned. Courts afford appraisal awards a strong presumption of validity to discourage endless litigation. An award can only be vacated under highly exceptional circumstances, which require meeting a very high legal burden of proof:

-

- Fraud: Clear evidence that one party intentionally lied, fabricated evidence, or manipulated the appraisal panel.

-

- Material Mistake: A profound, objective error in the award (e.g., valuing a completely different building or applying an incorrect mathematical formula that altered the outcome by a massive margin).

-

- Appraiser or Umpire Bias: Proving that the “disinterested” appraiser or neutral umpire had an undisclosed financial relationship or ongoing business conflict with one of the parties.

Because challenging an award is incredibly difficult and expensive, policyholders must get the process right the first time by hiring a Claim Settlement Expert to manage the claim from day one.

How do state-specific rules affect the appraisal process?

The rules governing appraisal vary dramatically depending on where your commercial property is located:

-

- Texas: Under the Texas Insurance Code, if a carrier pays an appraisal award, they may still be liable for statutory interest penalties under the Prompt Payment of Claims Act if they unreasonably delayed the claim before appraisal was invoked.

-

- Florida: Florida courts strictly enforce the “disinterested” standard for appraisers, often disqualifying anyone with a financial stake in the claim. Additionally, Florida litigation rules frequently require all coverage disputes to be resolved before an appraisal can be demanded.

-

- Colorado: The Colorado Supreme Court has issued landmark rulings outlining strict guidelines for appraiser impartiality, holding that appraisers must act as objective valuation experts rather than aggressive advocates.

-

- Statute of Limitations: In many states, the statute of limitations continues to run during the appraisal process. If your deadline is approaching, you must file a protective lawsuit to preserve your legal rights while the appraisal is conducted.

Why should commercial policyholders hire a public adjuster for claims over $250,000?

For claims exceeding $250,000, the complexity of commercial property damage—coupled with the sophisticated tactics deployed by insurance carriers—makes professional representation an absolute necessity.

When you hire a licensed public adjuster early in the process, they will:

-

- Conduct a comprehensive, independent forensic evaluation of the property damage.

-

- Bring in specialized experts, including structural engineers, industrial hygienists, and commercial cost estimators.

-

- Carefully analyze your policy language to identify coverage opportunities and avoid appraisal traps.

-

- Handle all communications and negotiations with the carrier’s adjusters, ensuring your claim is documented to the highest legal and technical standards.

To learn more about how a public adjuster can level the playing field, read When Should a Policyholder Hire a Public Insurance Adjuster?.

Why Insurance Appraisal Requires Significant Reform

The insurance industry often portrays appraisal as a fast, cost-effective alternative to litigation. In reality, many policyholders discover that appraisal is neither inexpensive nor fair, particularly in large commercial property claims where the financial stakes are highest.

While appraisal was originally intended to resolve minor disagreements over valuation, it has evolved into a process that frequently benefits insurers more than policyholders. Rather than providing a level playing field, appraisal can shift significant costs and risks onto the insured while allowing the insurance company to preserve many of its defenses even after an award is issued.

Top Reasons Appraisal Is Bad for Policyholders

1. The Process Is Expensive

Policyholders must typically pay for their own appraiser and share the cost of the umpire. Depending on the complexity of the claim, appraisal expenses can range from several thousand dollars to tens of thousands of dollars.

For many claims, the costs of appraisal can consume a substantial portion of any additional recovery, making the process economically impractical.

2. Insurers Can Still Deny Coverage After the Award

Perhaps the most misunderstood aspect of appraisal is that a “binding” appraisal award does not necessarily require the insurer to pay the full amount awarded.

Most policies reserve the insurer’s right to assert coverage defenses even after appraisal concludes. As a result, policyholders may spend months and thousands of dollars obtaining an appraisal award only to have the insurer deny all or portions of the claim based on exclusions, limitations, deductibles, or other coverage arguments.

3. The Process Focuses on Price, Not Accountability

Appraisal determines the amount of loss—not whether the insurer conducted a proper investigation, complied with claim handling requirements, or acted reasonably during the adjustment process.

Important issues such as claim delays, inadequate inspections, overlooked damages, and bad-faith conduct are often excluded from consideration.

4. Policyholders Lose Significant Leverage

Once appraisal is invoked, the focus shifts away from the insurer’s conduct and toward a narrow valuation dispute. This frequently reduces pressure on the carrier to negotiate fairly and can limit the policyholder’s ability to challenge other aspects of the claim.

5. There Is Little Meaningful Oversight

Unlike a courtroom proceeding, appraisal generally lacks formal discovery, evidentiary rules, judicial oversight, and appeal rights. A two-person agreement between one appraiser and the umpire can establish a binding award with very limited opportunity for review.

6. Appraisal Often Rewards the Party With Greater Resources

Large insurance carriers participate in appraisal proceedings regularly and often rely on the same appraisers, consultants, engineers, and attorneys. Most policyholders encounter the process only once, creating an inherent experience imbalance.

7. The Process Can Delay Final Resolution

Despite being promoted as a quicker alternative to litigation, appraisal can take many months to complete, especially when disputes arise regarding appraiser selection, umpire appointment, scope of damages, or award interpretation.

A Better Alternative

If appraisal is going to remain part of property insurance policies, significant reforms should be considered.

Potential reforms include:

-

Mandatory flat-fee caps on appraisal costs.

-

Cost shifting to the insurer when the appraisal award substantially exceeds the carrier’s estimate.

-

Strict deadlines for completion.

-

Binding payment obligations once an award is issued.

-

Independent oversight of appraisers and umpires.

-

Any expert expenses spent on the insurer’s side to be equally and fairly extended to the policyholder as well.

-

Consumer disclosure requirements explaining the risks before appraisal begins.

Most importantly, appraisal should be reserved for relatively small valuation disputes where the amount in controversy justifies the expense. For large commercial losses involving hundreds of thousands or millions of dollars, policyholders deserve a process that provides meaningful due process, transparency, accountability, and judicial oversight.

Until those reforms occur, policyholders should carefully evaluate whether appraisal truly serves their interests before agreeing to participate.

Can the Appraisal Process Be Fixed?

Proponents of appraisal often argue that the process simply needs reform rather than elimination. While there are certainly measures that could improve transparency, accountability, and fairness, many of the fundamental problems remain difficult to overcome.

If appraisal is going to continue as a dispute resolution mechanism, several significant reforms should be considered.

Require Licensing and Professional Standards

One of the most troubling aspects of the appraisal industry is the lack of consistent licensing and regulatory oversight. In many jurisdictions, individuals can perform appraisal services without holding an insurance license, public adjuster license, contractor license, engineering license, or any other professional credential.

This creates a troubling double standard. Insurance carriers frequently advocate for restrictions on contractors and other unlicensed individuals who assist policyholders with claims, often citing concerns about the unauthorized practice of public adjusting. Yet many of these same carriers routinely participate in appraisal proceedings involving individuals who operate with little or no regulatory oversight.

If appraisal is going to remain part of the claims process, appraisers and umpires should be subject to minimum licensing requirements, continuing education standards, ethical obligations, and meaningful disciplinary oversight.

Establish Clear Rules of the Road

Unlike litigation, appraisal often operates under vague policy language with few procedural safeguards. There are typically no uniform rules governing deadlines, disclosures, communications, conflicts of interest, or evidence submission.

Legislatures should establish clear statutory guidelines that define:

-

Timelines for initiating and completing appraisal.

-

Qualifications for appraisers and umpires.

-

Disclosure requirements for prior relationships and potential conflicts.

-

Standards for evidence and documentation.

-

Procedures for resolving procedural disputes.

-

Consequences for noncompliance.

Without clear rules, appraisal frequently devolves into a process where outcomes depend more on the participants involved than on any consistent set of standards.

Require Reporting and Regulatory Oversight

Currently, most appraisal proceedings occur with little or no regulatory visibility. State insurance departments generally have limited information regarding:

-

How often appraisal is invoked.

-

Which party invokes appraisal.

-

Award amounts.

-

Carrier payment practices following appraisal.

-

Frequency of disputes over appraisal awards.

-

Repeat use of specific appraisers or umpires.

Mandatory reporting would allow regulators to identify patterns of abuse, monitor outcomes, and better understand whether appraisal is functioning as intended.

Impose Penalties for Bad-Faith Conduct

One of the most significant shortcomings of appraisal is the absence of meaningful consequences for improper conduct.

There should be statutory penalties when parties:

-

Intentionally delay the appraisal process.

-

Withhold relevant information.

-

Engage in undisclosed conflicts of interest.

-

Misrepresent facts or damages.

-

Use appraisal as a tactic to avoid proper claim investigation.

-

Refuse to honor legitimate appraisal awards.

Without accountability, the incentives for gamesmanship remain intact.

The Fundamental Problem Remains

Even if these reforms were adopted, a larger question would remain: Why should policyholders be required to pay thousands of dollars to resolve disputes that often arise because an insurer failed to properly evaluate the claim in the first place?

Appraisal was originally intended to address limited disagreements over valuation. Over time, however, it has evolved into a costly quasi-judicial process that lacks many of the safeguards found in traditional litigation while producing outcomes that may still be challenged on coverage grounds.

The irony is difficult to ignore. The insurance industry frequently argues that strict licensing requirements are necessary to protect consumers from unqualified individuals assisting with claims. Yet the appraisal process often permits unlicensed and largely unregulated participants to determine the value of losses involving hundreds of thousands—or even millions—of dollars.

This inconsistency raises a fundamental question: If consumer protection truly matters, why are the individuals determining the value of major insurance claims often subject to fewer regulations than those assisting policyholders during the adjustment process?

For these reasons, meaningful reform may not be enough. While additional oversight and accountability would certainly improve the current system, the better solution may be to abolish appraisal altogether and replace it with a dispute resolution process that provides transparency, due process, regulatory oversight, and genuine consumer protections.

The appraisal industry often presents itself as a consumer-friendly alternative to litigation. Yet unlike judges, attorneys, public adjusters, insurance agents, and insurance companies, appraisal participants frequently operate with little regulatory oversight, no centralized reporting requirements, limited transparency, and few meaningful consequences for misconduct. Before expanding the role of appraisal in the insurance claims process, policymakers should first ask whether a system with so little accountability deserves such significant authority over the financial outcome of insurance claims.

The insurance appraisal process was designed to be a fair, efficient, and cost-effective way to resolve property valuation disputes. However, in the modern corporate landscape, major insurance carriers have increasingly turned this contractual tool into an accountability shield—using it to delay payments, avoid bad faith litigation, and pressure commercial policyholders into accepting undervalued settlements.

Conclusion: Is Appraisal Solving the Problem—or Hiding It?

Insurance appraisal was originally designed to resolve straightforward disagreements about the value of a covered loss. Over time, however, the process has expanded far beyond that limited purpose. Today, appraisal is frequently used in complex, high-dollar disputes involving competing experts, unresolved coverage issues, and significant disagreements over the scope of damage.

Supporters of appraisal often describe it as a faster, less expensive alternative to litigation. Yet many policyholders discover that the process can be costly, lacks meaningful oversight, permits unlicensed participants to influence major financial decisions, and may still fail to provide finality even after a “binding” award is issued.

Perhaps most troubling is that appraisal can shift attention away from the insurer’s claim handling conduct and focus almost exclusively on valuation. Questions about inadequate investigations, overlooked damages, unreasonable delays, and other claim handling concerns are often left unresolved while policyholders are asked to spend additional time and money pursuing an appraisal award.

If appraisal is going to remain part of the insurance claims process, substantial reforms are needed. Licensing requirements, regulatory oversight, reporting obligations, standardized procedures, transparency requirements, and meaningful penalties for misconduct should be the minimum standard—not the exception.

Until those reforms occur, policyholders should approach appraisal with caution. Before invoking appraisal, policyholders should carefully consider whether the process truly serves their interests.

A dispute-resolution system that lacks meaningful oversight, shifts costs to policyholders, permits unlicensed participants, and allows insurers to preserve coverage defenses even after a “binding” award deserves closer scrutiny from regulators, lawmakers, and the public.

If appraisal is truly designed to protect policyholders, why does it so often require them to spend their own money, navigate an unregulated process, and accept an outcome that the insurer may still challenge?

At Insurance Claim Recovery Support LLC (ICRS), we do not let carriers hide behind procedural shields. As a premier, Texas-based public adjusting firm, we represent commercial property owners, multifamily operators, HOAs, industrial facilities, and institutional building managers across multiple states. We specialize in maximizing settlements, reducing delays, and holding insurance companies fully accountable to their policy obligations.

If your commercial property has suffered a major loss and you are facing a massive valuation gap with your insurer, do not navigate this complex process alone. Contact the dedicated advocates at Insurance Claim Recovery Support LLC today to secure a professional Public Adjuster for Insurance Claims and ensure your property is fully and fairly restored.