Why Commercial Property Owners Need an Insurance Claim Guide

An Insurance claim guide is essential for navigating the complex process of recovering from property damage. For owners of commercial buildings, multifamily complexes, or religious institutions, understanding how to file and negotiate a claim can prevent significant financial loss.

Quick Answer: The 5 Key Stages of a Commercial Property Insurance Claim

- Report the Loss – Notify your insurer immediately after damage occurs.

- Document Everything – Take photos, videos, and create detailed inventories.

- Mitigate Further Damage – Take reasonable steps to prevent additional losses.

- Work with Adjusters – Understand that company adjusters represent the insurer, not you.

- Review & Negotiate Settlement – Carefully evaluate offers and negotiate for fair compensation.

Why This Matters for Commercial & Multifamily Property Owners ��

The stakes for commercial properties are high. With research showing 10% of claims are wrongfully denied and 40% of owners receive low payouts, going it alone is risky. Insurance companies employ adjusters to protect their bottom line, often using tactics like misclassifying damage or dragging out the process to justify lower settlements. These tactics can cost you hundreds of thousands of dollars on large fire, hurricane, or freeze damage claims.

I’m Scott Friedson, CEO of Insurance Claim Recovery Support. As a public adjuster, I’ve spent 15 years successfully settling large-loss commercial claims, often increasing recoveries by 30% to more than 3,800%. Proper claim management and policyholder advocacy can turn denied or underpaid claims into fair settlements—often avoiding unnecessary litigation entirely.

The Ultimate Insurance Claim Guide for Property Owners

When disaster strikes your commercial or multifamily property, you don’t have to steer the confusing insurance claim process alone. This Insurance claim guide walks you through every step, from understanding your policy to negotiating a fair settlement for perils like fire, hurricanes, tornadoes, wind, and freeze damage in Texas and nationwide.

Before You File: Understanding Your Commercial Policy

Most property owners don’t read their policy until they need it, but the fine print is critical. Before a loss, review this legally binding contract.

- Declarations Page: Your policy’s summary. It lists coverage limits, deductibles, and endorsements.

- Coverage Types & Exclusions: Your policy specifies what’s covered (fire, wind, etc.) and what isn’t. Flood damage is a common exclusion, requiring a separate policy, especially in flood-prone Texas areas like Houston or Corpus Christi.

- Endorsements: These modify your policy. “Ordinance and Law” coverage is vital for older buildings, as it pays to rebuild to current codes.

- Replacement Cost Value (RCV) vs. Actual Cash Value (ACV): RCV pays to replace with new materials, while ACV pays the depreciated value. The difference can be hundreds of thousands of dollars. RCV is worth the higher premium.

- Deductibles: This is your out-of-pocket cost. For wind/hurricane damage, percentage deductibles are based on the property’s total insured value, not the loss amount. A 2% deductible on a $2M property is $40,000.

Understanding your policy is the foundation for handling Large Loss Claims. The principles for Successful High Value Homes Insurance Claims apply here: preparation is everything.

Step-by-Step: How to File a Successful Property Damage Claim

When property damage occurs, your response in the first hours can dramatically affect your settlement. Follow these steps:

- Notify Your Insurer Immediately: Policies require prompt notification. In Texas, insurers have 15 days to acknowledge your claim. Delays can risk your coverage.

- Mitigate Further Damage: This is required by your policy. Tarp damaged roofs, shut off water to burst pipes, and keep all receipts for these emergency repairs.

- Document Everything: Before cleaning up, take extensive photos and videos of all damage. Create a detailed inventory of damaged items (building components, equipment, inventory) with as much detail as possible.

- Keep a Claims Diary: Record every call, email, and meeting. Note who you spoke with, what was discussed, and any deadlines. This creates an indisputable timeline.

- Obtain Detailed Repair Estimates: Get multiple bids from licensed contractors to establish a fair market value for repairs. Don’t feel pressured to use the insurer’s recommended contractors.

For peril-specific advice, see our guides on How to File an Insurance Claim for Fire Damage and Storm Insurance Claims: A Step-by-Step Guide.

The Adjuster’s Role: Company Adjuster vs. Public Adjuster

Not all adjusters work for you. Understanding their roles is key.

| Adjuster Type | Who They Work For | Their Objective | Who Pays Them |

|---|---|---|---|

| Company Adjuster | The Insurance Company | Protect the insurer’s financial interests; minimize payout | The Insurance Company |

| Independent Adjuster | Multiple Insurance Companies | Protect the insurer’s financial interests; minimize payout | The Insurance Company |

| Public Adjuster | The Policyholder | Maximize the policyholder’s settlement; advocate for you | The Policyholder (contingency fee) |

The company adjuster sent by your insurer works to protect their employer’s bottom line, not maximize your payout.

A public adjuster works exclusively for you, the policyholder. Our sole objective is to document your losses, interpret your policy, and negotiate with the insurer to secure the maximum settlement you deserve. For any significant commercial loss—like a fire in a Dallas apartment complex or hurricane damage in Houston—a public adjuster is invaluable. Policyholders with public adjusters often receive significantly higher settlements.

Crucially, a public adjuster can help you avoid unnecessary litigation. By presenting a professionally prepared claim, we resolve disputes through negotiation, saving you time, stress, and legal fees. Learn more about Public Insurance Adjusters: When to Hire One and Why and why it’s best to Engage Public Adjusters Early in Large Loss Claims.

Navigating the Settlement: Reviewing Offers and Avoiding Pitfalls

The settlement offer is a critical moment. Don’t rush it.

- Review Offers Carefully: Compare the insurer’s offer line-by-line with your own estimates and inventory. The first offer is rarely the best.

- Recognize Underpayment Tactics: Insurers may misclassify damage (e.g., “wind-driven rain” vs. wind damage), propose cheaper materials, or blame “wear and tear” to reduce payouts. Be aware of these 8 Sneaky Tricks Insurance Companies Use to Underpay and Delay Your Claim.

- Negotiate Strategically: Be organized and professional, but remember the adjuster is not your friend. Never sign a “final payment” release unless you are certain the offer is fair. Learn How to Negotiate with Insurance Adjuster for Property Damage.

- Watch for Delays: Intentional stalling is a red flag and may be a bad faith practice designed to make you accept a low offer out of frustration.

When Claims Go Wrong: Disputes, Appraisal, and Litigation vs. Public Adjuster Support

If your claim is denied or unreasonably delayed, you have options. Common denial reasons include policy exclusions, missed deadlines, or insufficient documentation.

When you disagree with the settlement, you can choose between several paths:

- The Appraisal Process: A method to resolve disputes over the amount of loss, but not coverage questions. Each side hires an appraiser, and they select a neutral umpire to determine the value.

- The Litigation Route: Filing an insurance claim lawsuit is a last resort. It is adversarial, expensive, and can take years. While it can force an insurer to pay, it involves significant legal fees. In Texas, the statute of limitations is often short, so timely action is critical if you pursue a Bad Faith Insurance Claim Texas.

- The Public Adjuster Approach: This is the proactive, cost-effective solution. We build a thoroughly documented claim to prevent disputes from the start. Our goal is to negotiate a fair settlement directly with the insurer, maximizing your recovery faster and without the high cost and stress of a lawsuit. Engaging a public adjuster early often prevents the need for litigation entirely. We can resolve most disputes without needing to ask What Kind of Lawyer Do I Need for Property Damage?.

Property Claim FAQs & Fact vs. Myth: Your Quick Insurance Claim Guide

Here are quick answers to common questions and myths for commercial property owners.

Common Questions from Property Managers

- How will a claim affect my premiums? While it can have an impact, the cost of not filing a legitimate claim for an “act of God” event like a hurricane almost always far exceeds any potential premium increase.

- What are typical claim timelines? In Texas, insurers have set deadlines to respond, but large commercial claims involving major fire or storm damage can take months to resolve properly.

- What is Loss of Rents coverage? Often called Loss of Use, this critical coverage for multifamily properties reimburses you for lost rental income when units become uninhabitable due to a covered peril.

- Is flood damage covered? No. Standard commercial policies exclude flood damage. You need a separate policy from the National Flood Insurance Program.

Fact vs. Myth

- MYTH: The insurance company’s adjuster works for you.

-

FACT: The company adjuster works for the insurer to minimize the payout. A public adjuster works only for you.

-

MYTH: You must accept the first settlement offer.

-

FACT: Initial offers are negotiable starting points. You have the right to negotiate for a fair amount based on your documented losses.

-

MYTH: If your claim is denied, it’s over.

-

FACT: A denial is a negotiating position. You can appeal, enter appraisal, or hire a public adjuster to re-present your claim.

-

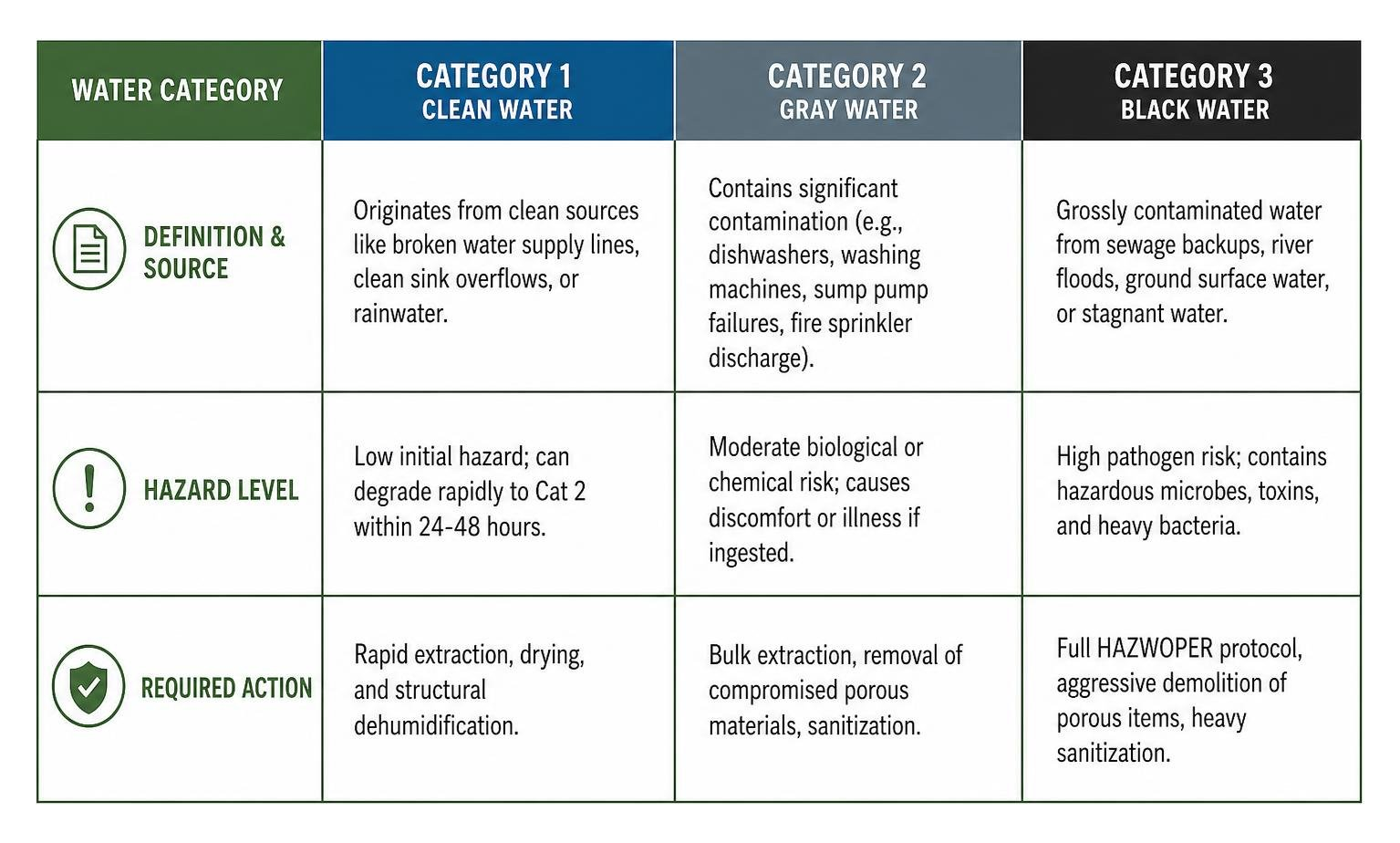

MYTH: All water damage is covered.

- FACT: Coverage depends on the source. A burst pipe is typically covered; external flooding is not.

Maximize Your Recovery and Rebuild with Confidence

The key takeaway from this Insurance claim guide is that you don’t have to steer this complex process alone, and you deserve the full value of your policy.

Proactive claim management—from understanding your policy to carefully documenting your loss—is essential. However, the insurance claims process is deliberately complex, designed to favor the insurer. When you’re dealing with a fire-damaged Dallas apartment complex or hurricane destruction in Houston, you need an expert advocate.

As public adjusters, we level the playing field. Insurance Claim Recovery Support has increased settlements by 30% to over 3,800% for commercial and multifamily property owners across Texas and nationwide. We are skilled negotiators who build unassailable claims to maximize your recovery, often resolving disputes without the time, stress, and cost of litigation.

Your property is your investment. We ensure you get the settlement you need to rebuild with confidence. Don’t let a lowball offer determine your future. Contact a Property Damage Public Adjuster for a Free Claim Review today and let us turn your policy into the protection it was meant to be.