When Your Insurer Won’t Pay: What Every Commercial Property Owner Needs to Know

Denied & Underpaid Insurance Claims are one of the most costly and disruptive challenges facing commercial and multifamily property owners today — and if you’re dealing with one right now, here’s what you need to know immediately:

Quick Answer: What To Do About a Denied or Underpaid Commercial Property Claim

- Get the denial in writing — request a formal written explanation citing the exact policy language used to justify the decision

- Review your policy — compare the denial reason against your actual coverage, exclusions, and endorsements

- Document everything — photos, videos, contractor estimates, expert reports, and all insurer communications

- Don’t cash a final settlement check without legal or professional review — doing so may limit your options

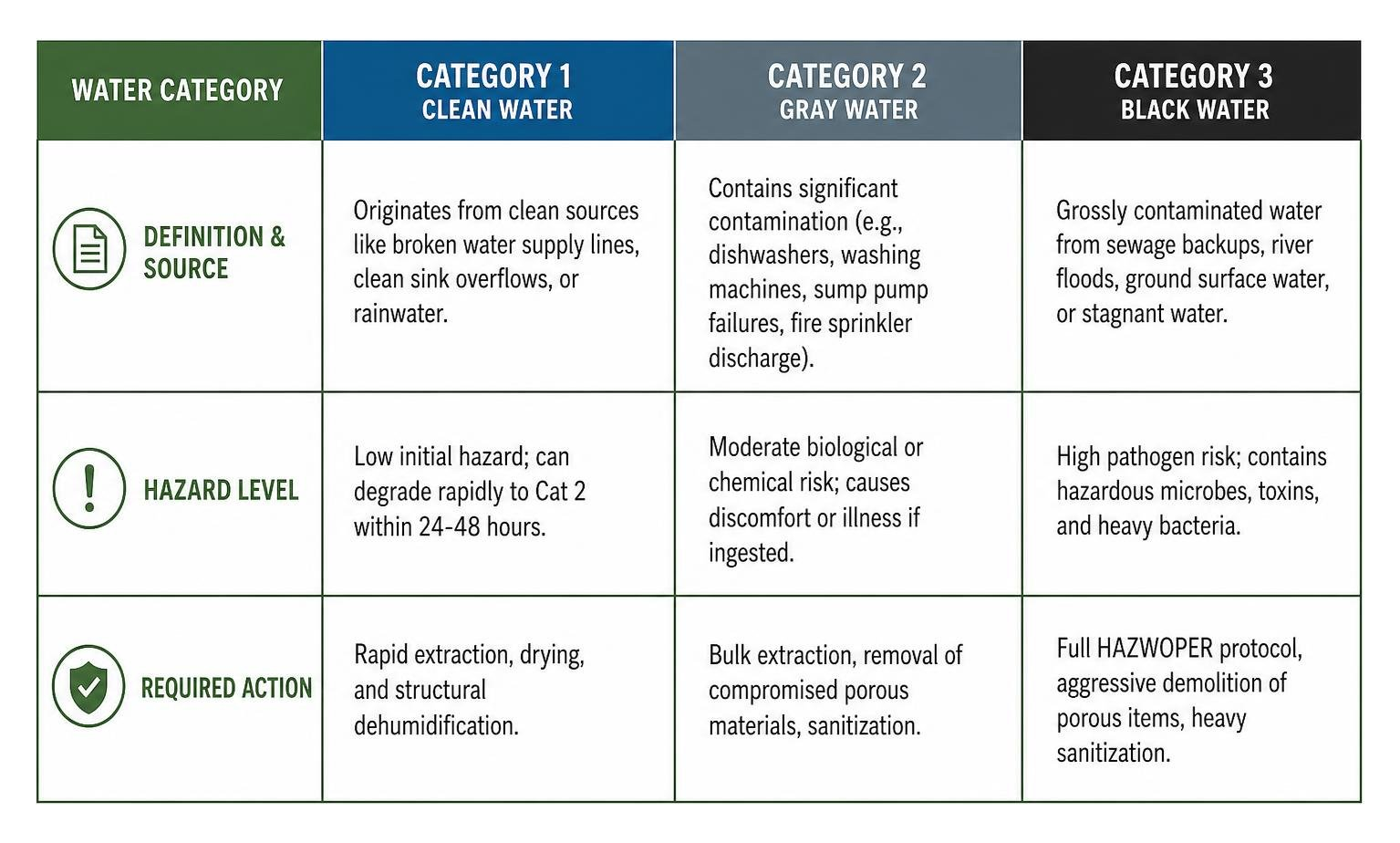

- Engage a licensed public adjuster — especially for large-loss commercial claims over $250,000, where professional advocacy consistently produces significantly higher settlements

- Know your deadlines — appeal windows are typically 30–60 days from the denial date, and state-specific statutes (like Texas Insurance Code 541 and 542) impose strict timelines

- Escalate if necessary — file a complaint with your state’s Department of Insurance, or consult an attorney if bad faith is suspected

Here is an uncomfortable truth about the insurance industry: carriers are for-profit businesses, and every dollar they don’t pay you goes directly to their bottom line. That profit motive shapes how claims are handled at every level — from the adjuster who shows up at your property to the corporate guidelines that determine what gets approved and what gets denied.

The numbers tell the story. Across U.S. marketplace plans, insurers denied roughly 18% of in-network claims in 2023, according to KFF and CMS data. Meanwhile, 80% of properly appealed claims succeed — yet fewer than 1% of policyholders ever file an appeal. That gap isn’t accidental. It’s the result of complex denial letters, tight deadlines, and a process designed to make fighting back feel overwhelming.

For commercial property owners — whether you operate an apartment complex, a retail center, an office building, or an industrial facility — the stakes are even higher. A denied or underpaid claim doesn’t just mean a repair bill. It means displaced tenants, lost revenue, lender pressure, and months of operational disruption while your insurer stalls.

This guide is here to change that dynamic.

I’m Scott Friedson, a multi-state licensed public adjuster and CEO of Insurance Claim Recovery Support (ICRS), with more than 15 years of experience resolving Denied & Underpaid Insurance Claims for commercial and multifamily property owners across the country. Over 500+ large-loss claims totaling more than $250 million, I’ve built a track record of overturning wrongful denials and recovering settlements that range from 30% to more than 3,800% above initial insurer offers — without unnecessary litigation.

Why Denied & Underpaid Insurance Claims Happen in Commercial Property

As we move through April 2026, the landscape for commercial property insurance has become increasingly adversarial. Insurers are no longer just “adjusting” claims; many are actively engineering outcomes to protect their quarterly earnings. This isn’t just a cynical viewpoint—it’s a reality reflected in recent federal scrutiny.

In May 2025, a U.S. Senate hearing led by Senator Josh Hawley highlighted what many in our industry have known for years: a pattern of “institutionalized fraud” characterized by the “delay, deny, underpay” strategy. The hearing exposed how some major carriers, particularly State Farm, have utilized non-licensed personnel and fragmented decision-making to distance the company from the actual damage on the ground. This trend is further evidenced by the Oklahoma Attorney General’s 2025 “Hail Focus Initiative,” which uncovered how carriers used predetermined outcomes and corporate savings targets to minimize payouts.

Regulatory investigations in California (led by the Commissioner and LA County) and Illinois have also targeted transparency issues and the improper application of deductibles. Even at the highest levels of government, these practices have faced backlash, including President Trump’s 2026 criticism of State Farm’s wildfire claim handling, which he described as a failure to honor commitments to policyholders.

For a business property insurance claim, the “underpayment” isn’t always a mistake. It’s often a calculated move. Carriers bet that multifamily operators, industrial facility owners, and retail center investors are too busy managing their assets to fight a multi-year battle. They use “corporate savings targets” to incentivize adjusters to bring in claims under a certain dollar amount.

Common Reasons for Denied & Underpaid Insurance Claims

Insurers have a playbook of “technicalities” they use to justify a Denied & Underpaid Insurance Claim. Understanding these is half the battle:

- Policy Exclusions: This is the most common hurdle. Insurers may claim that a loss was caused by “wear and tear” or “maintenance issues” rather than a sudden peril like hail or wind.

- Documentation Failure: If you don’t have “before” photos or a detailed inventory of the damage, the insurer will often default to a denial.

- Missed Deadlines: Commercial policies are notoriously strict. A delay in reporting a hail damage insurance process or a flood insurance claim process can lead to a total loss of rights.

- Cause of Loss Disputes: In complex cases like a fire insurance claims webinar might explain, insurers may argue that the damage was pre-existing or caused by an excluded secondary factor.

For more depth, see our Denied Insurance Claim Ultimate Guide.

Identifying Bad Faith in Denied & Underpaid Insurance Claims

“Bad faith” occurs when an insurance company violates its legal duty to act fairly and honestly toward its policyholders. It’s more than just a disagreement over price; it’s a systemic failure to uphold the contract.

Red Flags of Bad Faith:

- Unexplained Silence: If your adjuster stops responding to emails or calls for weeks at a time.

- Lowball Estimates: Offering a settlement that is so low it wouldn’t cover even 20% of the actual repair costs.

- Failure to Investigate: Sending an adjuster who spends 15 minutes on a 50,000-square-foot roof and concludes there is “no damage.”

- Serial Excuses: Constantly asking for the same documents or assigning a new adjuster every three weeks to “reset” the clock.

If you suspect these tactics, consult our Bad Faith Insurance Complete Guide.

Fact vs. Myth: Commercial Property Claim Realities

Myth: If I cash the check they sent, I can’t ask for more money. Fact: In most cases, you can still pursue supplemental payments if you discover more damage or if the initial payment was clearly an underpayment. However, you must be careful not to sign a “full and final release.”

Myth: The “Appraisal” process is a fast and fair way to settle. Fact: In Texas, 99% of appraisals are policyholder-initiated because the insurer’s offer was so low. These often result in significantly higher awards, frequently ranging from $10,000 to over $28,000 above the initial offer.

Myth: Most denials are legitimate. Fact: Statistics show that 80% of appealed claims succeed, yet only 0.2% of policyholders actually go through the effort to appeal. The system is designed to reward those who don’t fight back.

Need immediate assistance? Get Help with Denied Claim from our team.

Proven Strategies to Dispute and Overturn Unfair Decisions

When you are facing a Denied & Underpaid Insurance Claim, you aren’t just fighting for a check; you’re fighting for the survival of your business. At Insurance Claim Recovery Support, we specialize in a “settlement-first” approach. We aim to resolve claims through aggressive public adjusting services that force the insurer to acknowledge the truth of the damage.

Our USP is simple: we maximize settlements while avoiding the years-long delays of litigation or the unpredictability of appraisal. We maintain a 90% settlement success rate by bringing superior evidence to the table.

Public Adjuster vs. Litigation: Resolving Disputes Without Court

Many property owners think their only options are to accept the lowball offer or sue. There is a middle ground that is often much more effective for large-loss claims.

| Feature | Public Adjuster (ICRS) | Insurance Attorney |

|---|---|---|

| Primary Goal | Maximize Settlement via Evidence | Win Legal Judgment/Bad Faith |

| Timeline | Months | Years |

| Cost | Contingency Fee (usually lower) | Contingency + High Court Costs |

| Focus | Damage Assessment & Policy | Case Law & Litigation |

| Texas/Florida Cost | Non-litigated: ~$1.5k | Litigated: $10k+ |

Hiring a public adjuster needed for a claim over $250,000 is often the smartest financial move you can make. It levels the playing field against the insurer’s army of experts. If you’re wondering what is a public insurance adjuster hire, it’s essentially hiring a private “adjuster” who works exclusively for you, not the insurance company. While an inside property claims adjuster works for the carrier’s interests, we work for yours.

In some cases, you may eventually need a lawyer to fight insurance company tactics, but starting with a public adjuster ensures your evidence is rock-solid before you ever step foot in a courtroom.

Essential Documentation for Overturning a Denial

In Denied & Underpaid Insurance Claims, the party with the best paper trail wins. You need to prove not just that there is damage, but that the damage was caused by the covered event and that the cost to fix it is “reasonable and customary.”

Your Documentation Checklist:

- High-Resolution Visuals: Photos and videos of the damage taken immediately after the loss.

- Expert Reports: Independent structural engineering reports or roof moisture surveys.

- Detailed Estimates: Not just a one-page quote, but a line-itemized estimate using industry-standard software like Xactimate.

- Communication Log: A record of every call, the name of the commercial claims adjuster, and a summary of what was said.

- Financial Records: For business interruption claims, you’ll need profit and loss statements to prove the financial impact of the damage.

For a deeper dive, check out How to Navigate Commercial Property Claims in 5 Easy Steps.

Texas and Florida: Navigating Local Insurance Legislation

If your property is in the Sunbelt, you are dealing with some of the most complex insurance laws in the country.

Texas Realities: In cities like Austin, Dallas, Houston, and San Antonio, we deal with “Texas Insurance Code” Chapters 541 and 542. These statutes are designed to protect you. Chapter 542 (the Prompt Payment of Claims Act) requires insurers to meet specific deadlines or face 18% interest penalties plus attorney fees. This is critical for property damage claims in Texas. Whether you are in Lubbock, San Angelo, Waco, or Lakeway, these state-wide protections apply.

Florida Realities: Florida has recently seen massive shifts in bad faith laws. Litigation costs in Florida for insurance disputes can average over $10,000, whereas a non-litigated resolution through a public adjuster often costs a fraction of that, typically around $1,500. If you need a property damage lawyer Texas or Florida, we can help facilitate that transition if a settlement cannot be reached.

The “Institutionalized Fraud” Factor: Recent investigations in California and Illinois have mirrored the concerns raised by President Trump in 2026 regarding State Farm’s wildfire claim handling. The common thread? Insurers are increasingly using “non-licensed personnel” to make final claim decisions, bypassing the expertise of the adjusters on the ground. This fragmentation makes insurance claims dispute assistance more vital than ever.

FAQ: Denied & Underpaid Insurance Claims Translation

Q: The adjuster said my roof only has “granule loss” and it’s not a functional failure. What does that mean?

- Translation: “We see the damage, but we’re going to call it ‘cosmetic’ so we don’t have to pay to replace the roof. We hope you don’t know that granule loss is the first stage of structural failure.”

Q: Why is my insurer asking for 5 years of maintenance records for a hail claim?

- Translation: “We are looking for any evidence of pre-existing wear and tear so we can deny the claim based on ‘lack of maintenance’ rather than the storm that just hit.”

Q: My insurer offered a settlement, but it’s $100,000 less than my contractor’s estimate. Is this normal?

- Translation: “Yes, it’s a ‘lowball’ offer. We are testing to see if you will accept a partial payment or if you have the professional help to prove our numbers are wrong.”

At Insurance Claim Recovery Support, we represent the “underdog” in these massive commercial disputes. Whether it’s a retail center in Bee Caves, an apartment complex in Fort Worth, or a warehouse in Houston, our mission is the same: to turn a Denied & Underpaid Insurance Claim into a fair and full recovery.

Don’t let your insurer dictate the value of your loss. You paid your premiums in good faith; it’s time for them to pay your claim in the same way. Reach out to us for a no-obligation consultation and let’s start the process of making them pay up.