When a Large Loss Hits, Your Insurance Company Has Experts — Do You?

A Public Adjuster (Large Loss Insurance Claims) is a state-licensed insurance professional hired exclusively by you — the policyholder — to document, prepare, and negotiate your property damage claim against your insurance company.

If you’re dealing with a major commercial or multifamily property loss right now, here’s what you need to know quickly:

🔑 Quick Answer: What a Public Adjuster Does for Large Loss Claims

| Question | Answer |

|---|---|

| Who do they represent? | You — the policyholder only, never the insurer |

| When should you hire one? | Immediately after a loss event — ideally within 24–72 hours |

| What claims qualify? | Commercial, multifamily, hospitality, or institutional losses typically exceeding $250,000 |

| How do they get paid? | Contingency fee (typically a percentage of the final settlement — no upfront cost) |

| Can they help after a denial? | ✅ Yes — even on denied, underpaid, or already-filed claims |

| Do they increase settlements? | ✅ Yes — policyholders with representation have received dramatically higher settlements |

When disaster strikes a commercial building, apartment complex, hotel, or institutional property, the aftermath is rarely simple. You’re managing displaced tenants, halted operations, contractor bids, lender requirements, and a claims process that was designed — and staffed — by your insurance company, not by you.

Here’s a reality that most policyholders don’t discover until it’s too late: the adjuster your insurance company sends to your property works for them, not for you. Their job is to evaluate your loss within the boundaries that protect their employer’s bottom line. Yours is to recover fully and get back to business.

That gap in representation is exactly where a public adjuster steps in — and for large, complex losses, that gap can mean the difference between a settlement that covers your actual damages and one that falls millions of dollars short.

The stakes are highest for commercial property owners, multifamily operators, hospitality groups, religious organizations, and institutional facilities. These claims involve forensic accounting, code-upgrade requirements, business interruption calculations, and policy language that can make or break a recovery — details that a single overworked insurance company adjuster, often brought in from out of state during a catastrophe, may simply miss or minimize.

I’m Scott Friedson, CEO of Insurance Claim Recovery Support (ICRS) and a multi-state licensed Public Adjuster (Large Loss Insurance Claims) with more than 15 years of experience successfully settling hundreds of millions of dollars in commercial and multifamily property damage claims across the country. Over 500+ large-loss claims totaling more than $250 million, I’ve seen every tactic insurers use to delay, underpay, or deny valid claims — and I’ve built ICRS around one mission: making sure you don’t leave a single dollar on the table. In this guide, I’ll walk you through exactly when and why to engage a public adjuster, what the process looks like, and how to protect yourself every step of the way.

Defining the Role of a Public Adjuster (Large Loss Insurance Claims)

In insurance, “adjusting” is the process of determining the value of a loss. However, not all adjusters are created equal. A Public Adjuster (Large Loss Insurance Claims) holds a fiduciary duty to the policyholder. This means we are legally and ethically bound to act in your best interest—a stark contrast to the adjusters sent by the carrier.

When a large loss occurs, the insurance company typically assigns a “company adjuster” (their employee) or an “independent adjuster” (a contractor they hire). Both are paid by the insurance company. Their primary loyalty is to the insurer’s bottom line, which often creates a massive conflict of interest. As we discuss in The Case for Engaging Public Adjusters Early in Large Loss Claims, bringing in your own expert early levels the playing field.

The Difference in Adjuster Loyalties

| Feature | Company/Staff Adjuster | Independent Adjuster | Public Adjuster |

|---|---|---|---|

| Who pays them? | The Insurance Company | The Insurance Company | You (The Policyholder) |

| Whose interest is priority? | The Insurer | The Insurer | Yours |

| Cost to you? | “Free” (included in premium) | “Free” (included in premium) | Contingency Fee |

| Goal? | Minimize claim payout | Resolve claim for insurer | Maximize settlement |

Insurance companies are for-profit entities. In 2026, the industry remains under heavy scrutiny for prioritizing profits over policyholder protection. When you hire us, you are hiring professional advocacy designed to counter the insurer’s inherent bias.

Fact vs. Myth: Public Adjuster Authority

Myth: “My insurance company’s adjuster is my friend and will make sure I’m taken care of for free.” Fact: While they may be polite, their job is to find reasons to limit the payout based on policy exclusions and depreciated values.

Myth: “Public adjusters can get me more than my policy allows.” Fact: We cannot change the legal limits of your policy. However, we ensure you receive 100% of every dollar you are entitled to—amounts that are frequently overlooked by carrier adjusters who lack the time or incentive to perform a forensic investigation.

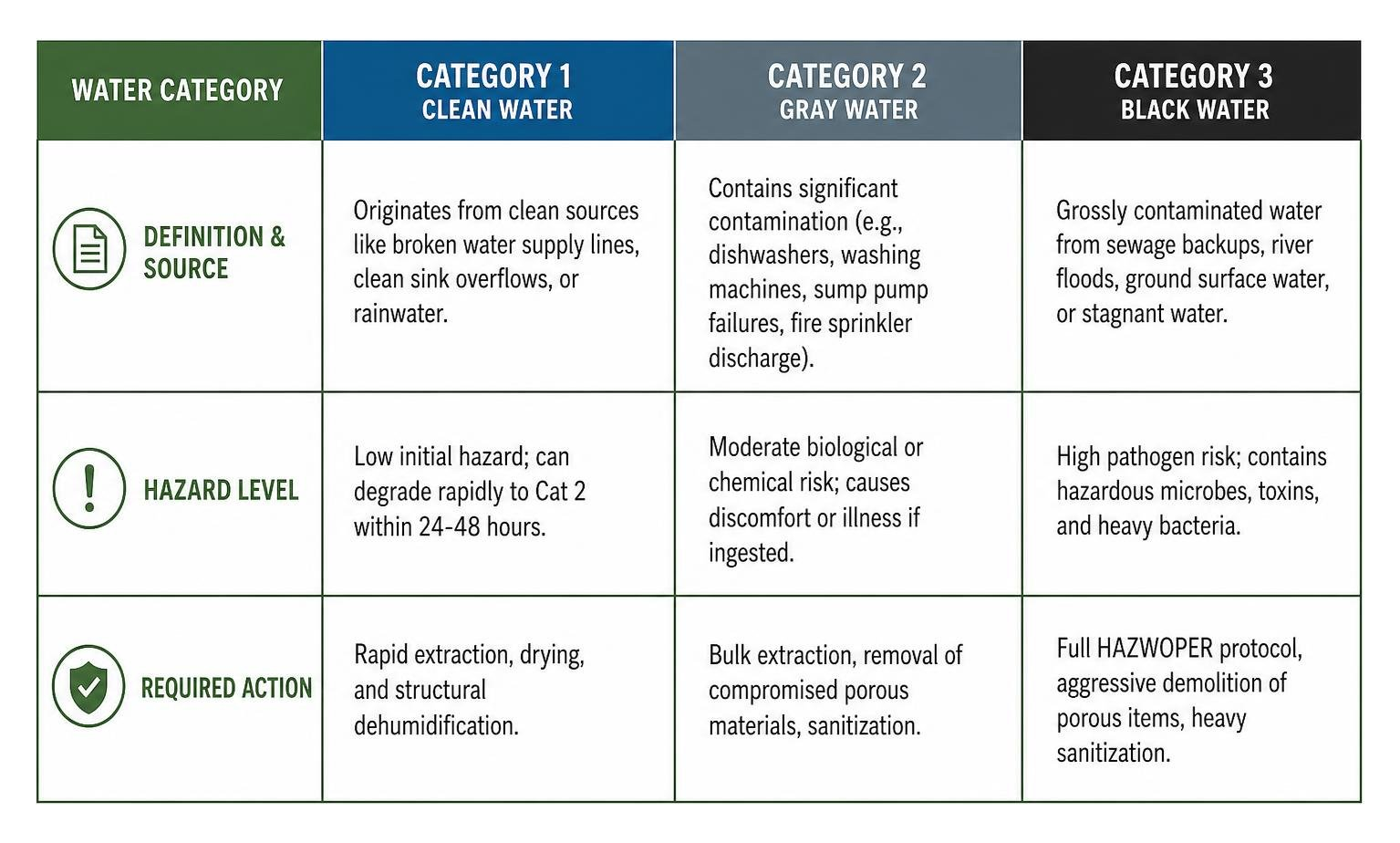

Identifying a Large Loss: Complexity Beyond Standard Claims

In the commercial sector, a “large loss” isn’t just a big bill; it’s a catastrophic disruption. Generally, we define a large loss as a claim exceeding $250,000, though for multifamily assets and industrial facilities, these figures quickly climb into the millions. You can learn more about these specifics in our guide: What is a Large Loss Claim?.

Why Commercial Claims Require a Public Adjuster (Large Loss Insurance Claims)

Commercial claims are exponentially more complex than residential ones. They require:

- Forensic Accounting: Calculating Business Interruption and “Extra Expense” coverage to keep your operations afloat.

- Building Code Compliance: Large losses often trigger “Ordinance or Law” requirements, meaning you must rebuild to current 2026 codes, not just “pre-loss” conditions.

- Specialized Scoping: Identifying hidden structural damage, air particulate contamination, or electrical compromises that aren’t visible to the naked eye.

Common Large Loss Scenarios in 2026

We frequently manage Storm Related Large Loss Claims across Texas and the Sunbelt. Common triggers include:

- Commercial Fire: The most devastating loss, involving smoke mitigation and structural integrity issues.

- Hurricane & Windstorm: Catastrophic damage to building envelopes and roofs.

- Frozen Pipe Bursts: A major issue in Texas (Austin, Dallas, Houston), where uninsulated commercial lines cause massive interior floods.

- Tornado Damage: Total loss scenarios requiring immediate triage.

")

Systemic Insurer Scrutiny and the 2026 Regulatory Landscape

The insurance industry is currently facing unprecedented pressure. Following a landmark May 2025 Senate hearing, lawmakers have begun investigating the “delay, deny, underpay” tactics used by major carriers. In Oklahoma, the ‘Hail Focus Initiative’ has set a precedent for holding insurers accountable, while California and Illinois have launched deep-dive investigations into unfair settlement practices.

Texas Insurance Code and Prompt Payment

In Texas, we have powerful tools to protect you. Texas Statute 541 prohibits unfair settlement practices, and Texas Statute 542 (the Prompt Payment of Claims Act) requires insurers to meet strict deadlines. If they fail to pay timely, they may owe you statutory interest and attorney fees.

Furthermore, a study by the Florida Legislature’s Office of Program Policy Analysis and Government Accountability (OPPAGA) showed that policyholders with public adjuster representation received settlements 747% higher for hurricane claims than those who went it alone. This data reinforces why professional advocacy is essential.

National Regulatory Trends

As of April 2026, political criticism of the insurance industry has reached a fever pitch, with even former President Trump weighing in on the “predatory” nature of modern premiums and claim denials. In Florida, litigation costs have skyrocketed, leading many carriers to attempt to force policyholders into the “Appraisal” process—a move we often help clients navigate to ensure fair valuation without the need for years of court battles.

Strategic Advocacy: The Large Loss Claims Process

Our approach is built on the Large Loss Team Right Resources model. We don’t just “look” at damage; we prove it.

Evidence-Based Documentation

We utilize high-tech tools to build an undeniable case:

- Thermal Imaging: To detect moisture behind walls and under roof membranes.

- Xactimate Estimates: Using the industry-standard software to provide line-by-line cost accuracy.

- Aerial Reports & Drones: For high-resolution documentation of roof and building envelope damage.

- Forensic Engineering: Bringing in structural experts to verify damage that carrier adjusters might dismiss as “wear and tear.”

Avoiding Litigation and Appraisal

Our goal is to get you paid fairly and fast. We maintain a 90% settlement success rate without the need for lawsuits. By providing the insurer with a “comprehensive proof of loss” early in the process, we make it difficult for them to justify a lowball offer. This strategic negotiation reduces delays and keeps you out of the courtroom.

Vetting Your Representative: Licensing and Fees

Hiring a Public Adjuster (Large Loss Insurance Claims) is a major business decision. In most states, including Texas and Florida, fees are capped (typically at 10% to 15% of the settlement) after a declared disaster.

Choosing a Reputable Public Adjuster (Large Loss Insurance Claims)

Don’t just hire the first person who knocks on your door. Look for:

- Multi-State Licensing: We are licensed in Texas, Florida, Georgia, and beyond.

- NAPIA Membership: Membership in the National Association of Public Insurance Adjusters signifies a commitment to ethics.

- BBB Rating: Check for a history of satisfied commercial clients.

Precautions After a Disaster

Be wary of “storm chasers” or contractors offering to “handle your claim.” In many states, it is unlawful for a contractor to act as an adjuster. Always verify that your representative is a licensed Public Adjuster. Most states allow you to cancel a contract via certified mail within a few business days if you feel pressured into signing.

Frequently Asked Questions about Large Loss Claims

Can a public adjuster help if my claim was already denied or underpaid?

Absolutely. We specialize in reopening claims that have been wrongfully denied or closed with insufficient funds. We perform a forensic re-evaluation of the property to find overlooked damage—like smoke particulates in HVAC systems or hail-damaged roof membranes—that the carrier’s adjuster “missed.”

How do public adjuster fees impact my final settlement?

While we work on a contingency fee, the “net recovery” for the policyholder is almost always significantly higher. If we increase your settlement by 392% (as seen in some wildfire cases) or 747% (per the OPPAGA study), our fee is a small investment compared to the massive increase in funds available for your rebuild.

What are the specific Texas regulations for commercial property claims?

Texas is a “bad faith” state. Under the Texas Department of Insurance (TDI) guidelines, you have specific rights regarding the timeline of your claim. We leverage Texas Statutes 541 and 542 to ensure the carrier doesn’t sit on your money while your business suffers.

Conclusion

Recovering from a large loss is a marathon, not a sprint. At Insurance Claim Recovery Support, we provide the endurance and expertise needed to cross the finish line with your business intact. With a 90% settlement success rate and a focus on commercial and multifamily advocacy, we ensure that the “experts” hired by the insurance company are met with even more qualified experts on your side.

If your commercial property in Austin, Dallas, Houston, San Antonio, or anywhere across our licensed states has suffered a major loss, don’t face the carrier alone.

Contact a Public Adjuster for a Free Claim Review today and let us start building your recovery.