Filing a Large Loss Hail Damage Insurance Claim: Why Every Hour Counts

A large loss hail damage insurance claim is one of the most financially consequential events a commercial property owner, multifamily operator, or institutional facilities manager will ever face — and the window to act correctly is narrow.

Quick Answer: How to File a Large Loss Hail Damage Insurance Claim Fast

- Document immediately — Photograph and video every affected surface within 24–48 hours of the storm, including rooftop systems, HVAC units, gutters, skylights, and siding.

- Secure official weather data — Pull National Weather Service storm reports to confirm hail size, date, and geographic path over your property.

- Notify your insurer in writing — Report the loss promptly; many commercial policies impose strict reporting windows.

- Do not begin permanent repairs — Temporary weatherproofing is appropriate, but permanent repairs before documentation can void portions of your claim.

- Get an independent professional inspection — Do not rely solely on the carrier’s adjuster. Commission your own licensed inspector or public adjuster before the insurance company’s CAT team sets the scope.

- Invoke the appraisal provision early if needed — If the insurer’s estimate is significantly lower than your independent contractor’s assessment, the appraisal process is your fastest path to resolution without litigation.

The scale of hail losses in North America has reached a breaking point for the insurance industry — and for commercial policyholders caught in the middle. In 2024 alone, the NOAA recorded 5,373 hail events across the United States, and U.S. roof-related insurance claims reached nearly $31 billion, a 30% increase since 2022. State Farm alone paid out more than $5.6 billion in hail-related claims in 2025, with Texas leading at $1.4 billion. Across the border, a single August 2024 Calgary hailstorm generated $3.25 billion in insured losses and over 130,000 claims — making it the second-costliest disaster in Canadian history.

These numbers are not just statistics. They represent real commercial buildings with damaged TPO membranes, apartment complexes with compromised rooflines, hotels unable to rent rooms, and churches waiting months for a fair settlement. And behind many of those delayed or underpaid claims is a pattern of insurer behavior — cosmetic damage reclassifications, pre-existing damage arguments, and CAT team assessments that miss critical functional damage — that is now drawing scrutiny from regulators, state attorneys general, and even the U.S. Senate.

�� Key Takeaway: The average insurance payout for a hail damage roof claim ranged from $12,000 to $17,000 in 2024 — but for commercial and multifamily properties, losses routinely exceed $250,000. The gap between what insurers initially offer and what policyholders are actually owed can be staggering.

I’m Scott Friedson, CEO of Insurance Claim Recovery Support (ICRS) and a Multi-State Licensed Public Adjuster with more than 15 years of experience settling large loss hail damage insurance claims for commercial and multifamily property owners across the country. Over 500+ claims valued at more than $250 million, I’ve seen every tactic insurers use to minimize payouts — and I’ve developed proven strategies to overcome them.

Large loss hail damage insurance claim terms to know:

Defining the Large Loss Hail Damage Insurance Claim for Commercial Assets

In commercial insurance, not all claims are created equal. While a single-family home might suffer a few broken shingles, a large loss hail damage insurance claim involves complex building systems where the financial stakes start at $250,000 and often climb into the millions. These claims impact major assets like retail plazas in Houston, industrial warehouses in Fort Worth, and sprawling multifamily complexes in San Antonio.

When we talk about Hail Damage, we are looking at more than just visual pockmarks. We are looking at the total compromise of a building’s protective envelope. In 2026, the threshold for a “large loss” is typically defined by damage that exceeds standard coverage limits or requires the involvement of specialized “Large Loss” units within the insurance company.

Proving Functional Damage in a Large Loss Hail Damage Insurance Claim

The biggest hurdle in a commercial claim is the debate over “functional” versus “cosmetic” damage. Functional damage is anything that reduces the lifespan of the roof or its ability to shed water. This includes shingle bruising, fractures in TPO membranes, or the displacement of granules that protect the underlying bitumen.

Translation: If an adjuster tells you the damage is “cosmetic,” they are essentially saying, “We see the damage, but we don’t think it’s broken enough for us to pay for a replacement.”

According to 2024 NOAA data, hail events are becoming more violent, with stones frequently exceeding 2 inches in diameter. At that size, the impact energy is enough to shatter concrete tiles or create micro-fractures in metal seams that lead to slow, catastrophic leaks. We use “directional impact” markers—dents on the north side of HVAC vents or west-facing siding—to prove the storm’s path and correlate it with National Weather Service data.

The $250K+ Commercial Threshold

Large loss claims typically involve:

- Industrial Facilities: Where roof failure can destroy millions in inventory.

- Retail Plazas: Where multiple tenants are affected by interior leaks.

- Hospitality Assets: Where a dented roof isn’t just an eyesore; it’s a liability that can lead to mold and loss of room revenue.

For these properties, Hail Claims require a sophisticated approach that accounts for the unique materials involved, such as EPDM, TPO, and modified bitumen.

Critical Steps to Document Your Large Loss Hail Damage Insurance Claim

Speed is your greatest ally, but accuracy is your best defense. The moment the storm clears in Austin or Dallas, you must begin building your “evidence locker.”

The first step is establishing the “Date of Loss.” Insurers often try to argue that damage was “pre-existing” or occurred during a previous storm outside the policy window. By pulling immediate reports from the National Weather Service and cross-referencing them with on-site photos, you pin the carrier down. For more guidance, see our Dos and Don’ts of Filing Hail Claim Damages for Policyholders.

Professional Inspections vs. Carrier Adjusters

After a major storm, insurance companies deploy Catastrophe (CAT) teams. These are often out-of-state adjusters who may not be familiar with Texas building codes or the specific nuances of commercial roofing. There are often significant “licensing gaps” where the person inspecting your $10 million apartment complex in Lubbock usually handles small residential claims.

This is why Roof Hail Damage must be assessed by an independent engineer or a public adjuster who understands commercial assemblies. We look for “soft bruising” and structural compromises that a rushed CAT adjuster will almost certainly overlook.

Translation: “Pre-existing damage” is the insurer’s way of ignoring your current storm loss.

If your insurer claims the damage was already there, point to your most recent underwriting inspection or maintenance log. If you had a clean inspection six months ago, and now you have 2-inch pockmarks across your TPO roof, the “pre-existing” argument falls apart. Scientific research proves that while aged roofs are less resilient, a significant hail event causes new, distinct functional damage that is separate from ordinary wear and tear.

Overcoming Systemic Insurer Scrutiny in Large Loss Hail Damage Insurance Claims

In 2025 and 2026, the insurance industry has faced unprecedented scrutiny. A May 2025 Senate hearing highlighted how major carriers like State Farm have systematically reduced payouts for legitimate hail claims. This led to the Oklahoma Attorney General’s “Hail Focus Initiative” and similar investigations in California and Illinois.

Even President Trump, in early 2026, criticized the insurance industry for its treatment of property owners after major catastrophes, calling for more transparency in how claims are adjusted. For Texas owners, the question remains: Is Texas at War with Hail Damage Insurance Claims?

The 2026 Regulatory Landscape

The shift from flat-dollar deductibles to percentage-based deductibles has caught many commercial owners off guard. If your retail center is valued at $10 million and you have a 3% hail deductible, you are responsible for the first $300,000. Insurers know this and often write estimates just below that deductible amount to avoid paying anything at all.

| Feature | Flat Deductible | Percentage-Based Deductible (2-5%) |

|---|---|---|

| Cost Predictability | High (e.g., fixed $10,000) | Low (Fluctuates with property value) |

| Out-of-Pocket Risk | Lower | Potentially hundreds of thousands |

| Insurer Strategy | Standard adjusting | Often used to “zero out” claims |

Texas Insurance Code Statutes 541 and 542

In Texas, policyholders are protected by the “Prompt Payment of Claims Act”. These laws require insurers to acknowledge, investigate, and pay or deny claims within specific timelines. If they fail to do so, or if they engage in “unfair settlement practices,” they can be liable for statutory interest (currently 10% or more depending on the year) plus attorney fees. This is a powerful tool in any Hail Damage Claim Dispute.

Commercial and Multifamily Large Loss Hail Damage Insurance Claim: Beyond the Roof

A large loss hail damage insurance claim isn’t just about the roof. On a commercial building, the “collateral damage” can be just as expensive.

We frequently find that rooftop HVAC units, cooling towers, and chiller plants have had their aluminum fins crushed. This reduces the unit’s efficiency, leading to higher energy bills and eventual mechanical failure. In a multifamily setting, hail can shatter skylights and damage “soft metals” like gutters and window wraps. For a deeper look at these complexities, visit our page on Hail Claims.

Business Interruption and Extra Expense

For hotels in Waco or office buildings in Fort Worth, the physical damage is only half the story. If a hailstorm punctures a roof and causes interior flooding, you may lose the ability to rent space.

Translation: “Extra Expense” coverage is designed to pay for the costs of keeping your business operational while repairs are underway—such as renting temporary office space or industrial drying equipment. This is often the most under-claimed part of a large loss.

Avoiding Litigation in a Large Loss Hail Damage Insurance Claim

No property owner wants to end up in a legal battle. Litigation is slow, expensive, and disruptive to operations. The better path is resolving the claim correctly and completely before it ever reaches that point.

At ICRS, our focus is achieving favorable settlements without unnecessary litigation, and we’ve consistently resolved the vast majority of large loss claims through disciplined claim preparation and strategic advocacy.

How We Do It:

1. Public Adjuster Advocacy (Primary Strategy):

The single most important factor in a successful large loss claim is having experienced representation that understands both construction and policy language.

ICRS acts as your advocate throughout the entire process—developing a fully supported scope of loss, aligning it with policy coverage, and presenting it in the format carriers rely on (including Xactimate). This allows the claim to be evaluated and approved at higher levels within the insurance company—where real settlement authority exists.

We don’t just “negotiate”—we engineer the claim for approval.

👉 Learn more:

https://insuranceclaimrecoverysupport.com/claim-documentation-process

https://insuranceclaimrecoverysupport.com/common-hail-claim-mistakes

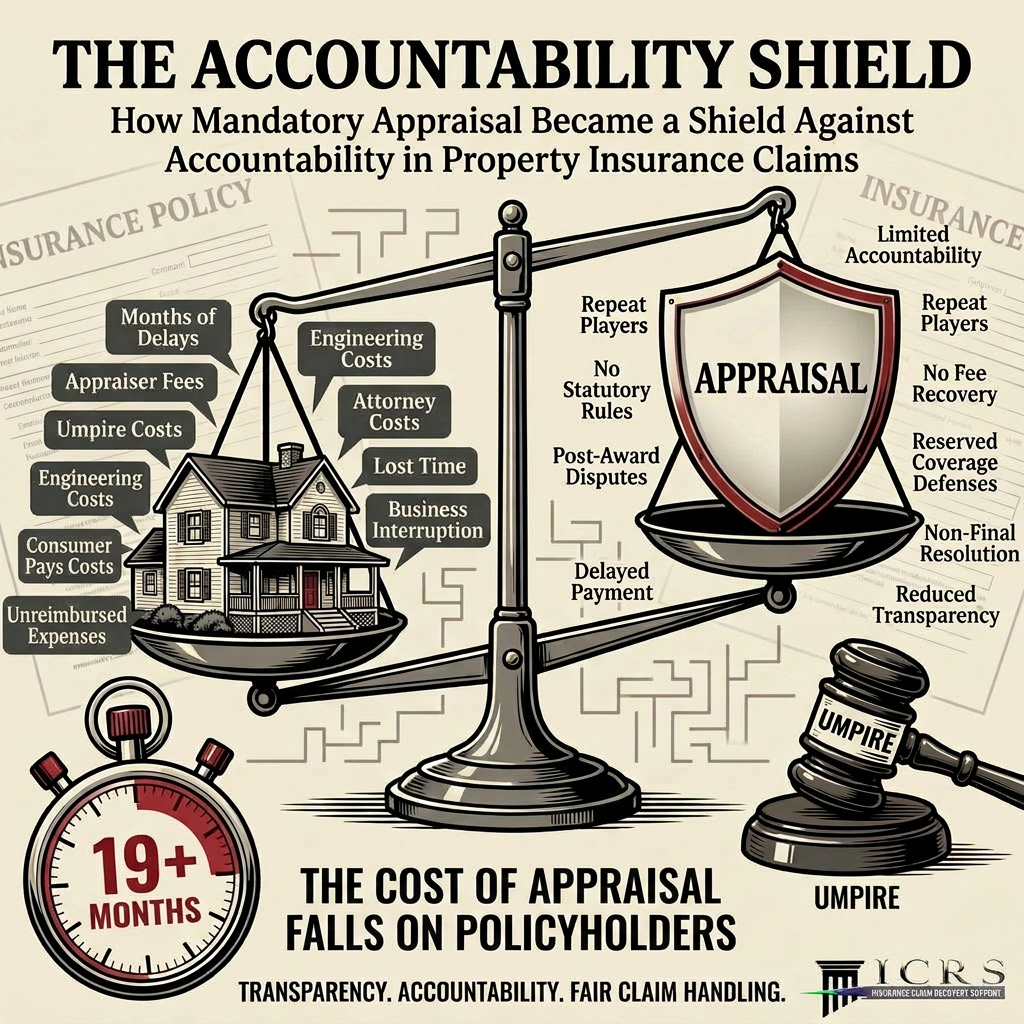

2. Appraisal (Strategic Tool, When Necessary):

Appraisal can help resolve scope and pricing disputes, but it is not a cure-all. If used too early, it can limit leverage and lock in an incomplete claim. When used correctly—after the claim is fully documented—it can help bring the claim to a defined resolution.

👉 Learn more about appraisal considerations:

Insurance Claim Appraisals: Where’s the Limit for Policyholders?

The bottom line:

Well-prepared claims get paid. Poorly prepared claims get delayed, disputed, or underpaid.The goal is not to fight the insurance company—it’s to present a claim so thoroughly supported that a fair settlement becomes the most logical outcome.

If you find yourself in a Hail Damage Claim Dispute, professional representation is often the only way to level the playing field.

FAQ: Navigating Your Large Loss Hail Damage Insurance Claim

What is the average payout for a commercial hail claim in 2026?

While residential claims averaged $12,000–$17,000 in 2024, commercial payouts in 2026 vary wildly based on square footage. For a mid-sized retail plaza or apartment complex, settlements typically range from $250,000 to over $1,500,000, depending on whether a full roof replacement and HVAC restoration are required.

How do percentage-based deductibles affect large loss settlements?

They can be devastating. A 2% deductible on a $20 million industrial warehouse means the owner pays $400,000 out of pocket. If the insurance adjuster “lowballs” the estimate at $450,000, the owner only receives $50,000 for a massive repair job. This is why getting an accurate, high-resolution damage scope is critical.

Can an insurer deny a claim based on “cosmetic” metal damage?

They try to, especially with metal roofs or siding. However, if the hail impacts have compromised the factory finish (leading to premature rust) or weakened the seams (leading to future leaks), it is functional damage. We fight these denials by proving the long-term structural impact of the “cosmetic” dents.

Conclusion: Securing Your Large Loss Hail Damage Insurance Claim Settlement

Navigating a large loss hail damage insurance claim is a marathon, not a sprint, but the first few steps determine if you’ll ever cross the finish line with a fair settlement. Whether you are managing a portfolio of apartments in Houston, a hospital in San Angelo, or a shopping center in Georgetown, the tactics used by insurers are the same. They rely on delays, complex policy language, and “cosmetic” exclusions to protect their bottom line.

Insurance Claim Recovery Support (ICRS) is here to protect yours. We are a licensed public insurance adjusting firm that represents policyholders only—never the insurance companies. We specialize in the complex, high-stakes world of commercial and multifamily property claims across Texas and the United States.

From the initial inspection in Lubbock to the final settlement negotiation in Dallas, our team advocates for your best interest. We don’t just find the damage; we prove it, price it, and push the carrier to pay it.

If you’ve suffered hail damage and want to ensure your claim is handled fast and fairly, don’t wait for the insurer to tell you what they think your loss is worth. More info about large loss services is just a click away. Let us help you recover what you’re rightfully owed.