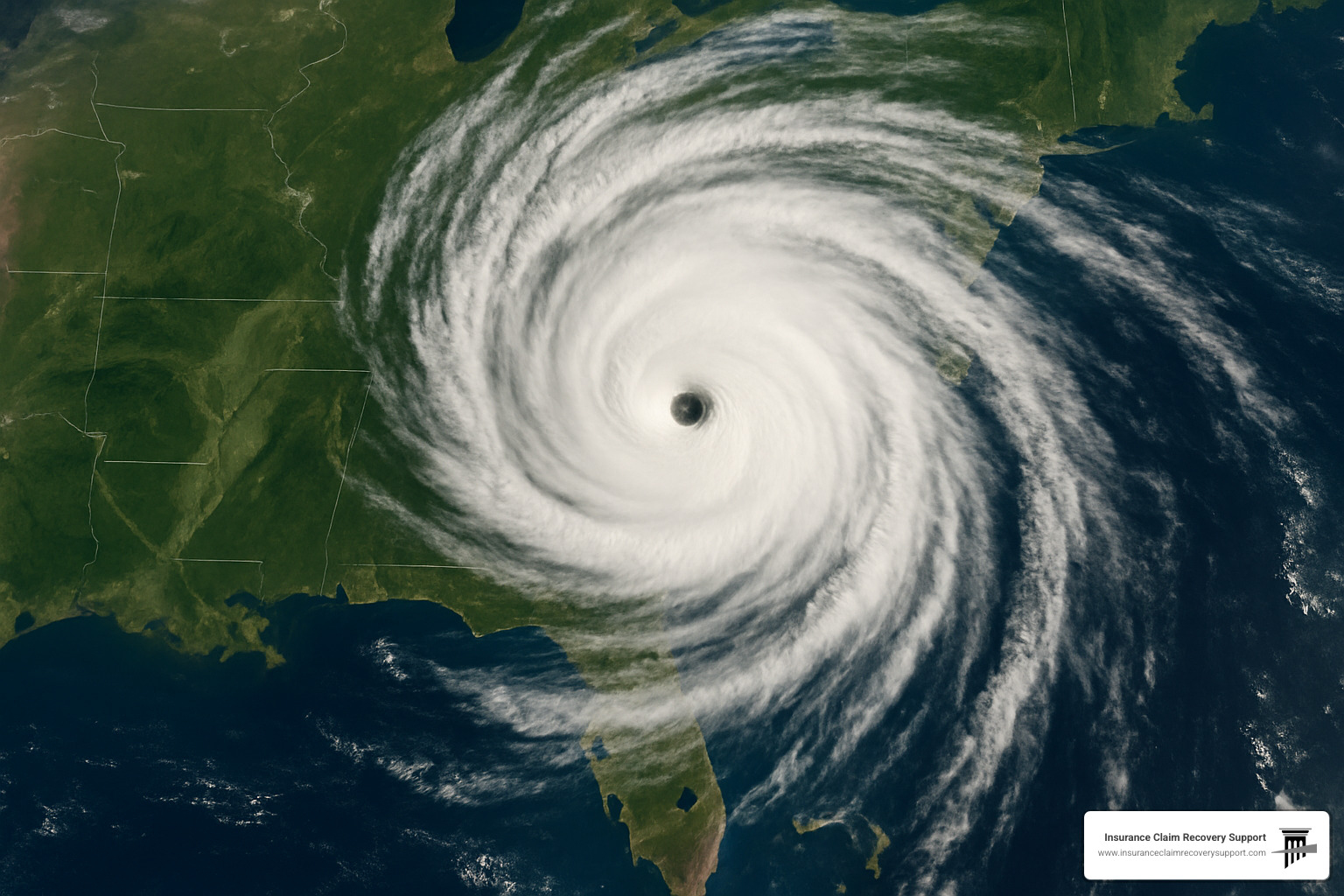

Why Understanding Hurricane Categories Could Save Your Property

The saffir simpson scale is a 1-to-5 rating system that classifies hurricanes based on their sustained wind speeds to estimate potential property damage. Here’s what you need to know:

The Five Categories:

- Category 1: 74-95 mph – Some damage to roofs, siding, and gutters

- Category 2: 96-110 mph – Extensive damage; major roof and siding loss

- Category 3: 111-129 mph – Devastating damage; well-built homes lose roofs

- Category 4: 130-156 mph – Catastrophic damage; severe structural damage

- Category 5: 157+ mph – Complete roof failure; total destruction possible

Key Facts:

- Categories 3-5 are considered “major hurricanes”

- Damage increases exponentially – a Category 2 storm causes roughly 10 times more damage than Category 1

- The scale measures only wind speed, not storm surge or rainfall

When Hurricane Harvey slammed into Texas as a Category 4 storm in 2017, it brought 130+ mph winds that caused catastrophic structural damage across the Gulf Coast. But here’s what many property owners don’t realize: the category only tells part of the story. Harvey’s unprecedented rainfall and flooding caused more damage than its winds in many areas.

For Texas property owners – whether you manage commercial buildings, multifamily complexes, or other facilities – understanding how the saffir simpson scale translates to real-world damage helps you prepare better and document losses more effectively when filing insurance claims.

I’m Scott Friedson, and over my career settling 500+ large loss claims valued at over $250 million, I’ve seen how misunderstanding the saffir simpson scale leads property owners to underestimate damage and accept lowball settlements. My experience with hurricane claims across Texas has shown me exactly how wind speed categories translate to actual structural damage and insurance coverage.

Understanding the Saffir-Simpson Hurricane Wind Scale

The Saffir-Simpson Hurricane Wind Scale might sound complicated, but it’s actually beautifully simple. Think of it as a straightforward 1-to-5 rating system that tells you exactly what kind of wind damage to expect from a hurricane.

Here’s what makes it work: the scale looks at only one thing – maximum sustained wind speeds measured over a 1-minute average at 33 feet above ground. No other factors, no complex calculations. Just pure wind speed translated into damage potential.

Back in 1971, civil engineer Herbert Saffir was studying low-cost housing in hurricane areas when he realized something important. People needed a simple way to understand what different wind speeds actually meant for their buildings. Working with meteorologist Dr. Robert Simpson (who ran the National Hurricane Center at the time), they created this wind-focused scale that property owners could actually use.

What every Texas property owner should understand is this: the saffir simpson scale works like a damage multiplier, not a simple ladder. When wind speeds jump from Category 1 to Category 2, the damage potential doesn’t just double – it can increase by ten times or more. That’s because wind power increases exponentially with speed.

When meteorologists talk about “major hurricanes,” they mean Categories 3, 4, and 5 – storms packing winds of 111 mph or higher. These are the storms that can make buildings uninhabitable for weeks or months.

Why Was the saffir simpson scale Created?

Before the saffir simpson scale existed, hurricane descriptions were frustratingly vague. Weather reports might say a storm was “intense” or “dangerous,” but what did that actually mean for your roof? Your windows? Your business operations?

Herbert Saffir faced this exact problem while working on building codes. He needed to predict how different structures would handle hurricane-force winds, but the existing storm descriptions were too general to be useful.

The solution was creating something as straightforward as the Richter scale for earthquakes. Just like you instantly know a 7.0 earthquake is much more serious than a 4.0, the hurricane scale gives you immediate context.

How Has the saffir simpson scale Evolved?

The original saffir simpson scale tried to do too much. Along with wind speeds, it included central pressure readings and storm surge predictions. Unfortunately, it created more confusion than clarity.

Here’s why: storm surge depends on much more than just wind speed. The shape of the coastline, the depth of the ocean floor, the size of the storm, and even the angle of approach all matter enormously.

Between 2009 and 2012, the National Hurricane Center made a smart decision. They stripped out everything except wind speed, focusing the scale on what it does best – predicting wind damage to structures.

The 2012 update also fixed a technical problem with converting between knots and miles per hour. Category 3 now tops out at 129 mph instead of 130, and Category 4 starts at exactly 130 mph.

Breaking Down the Five Hurricane Categories

When I explain the saffir simpson scale to property owners, I always emphasize one crucial point: the jump between categories isn’t just about higher numbers. Each step up represents an exponential increase in destructive power that can mean the difference between manageable repairs and total reconstruction.

| Category | Wind Speed (mph) | Typical Damage | Famous Examples |

|---|---|---|---|

| 1 | 74-95 | Some roof/siding damage, power outages | Humberto (2007) |

| 2 | 96-110 | Extensive roof damage, major outages | Ike (2008) |

| 3 | 111-129 | Devastating damage, well-built homes damaged | Alicia (1983) |

| 4 | 130-156 | Catastrophic damage, severe structural loss | Harvey (2017) |

| 5 | 157+ | Complete roof failure, total destruction | Andrew (1992) |

Category 1: 74-95 mph – “Some Damage”

Don’t let the word “some” fool you into thinking Category 1 hurricanes are gentle. I’ve processed plenty of six-figure insurance claims from these supposedly “minor” storms.

Roof shingles and siding take the biggest hit in Category 1 storms. Well-built homes typically survive with their structure intact, but you’ll likely see gutters torn away, tree limbs snapped, and power lines down. The outages usually last just a few days.

Hurricane Humberto in 2007 perfectly illustrates a Category 1 impact. While it didn’t make national headlines like stronger storms, it still caused millions in property damage across Texas.

Category 2: 96-110 mph – “Extensive Damage”

Category 2 storms earn their “extensive damage” label by affecting multiple building systems simultaneously. You’re not just dealing with missing shingles anymore – you’re looking at major roof structure damage and significant siding loss.

Mobile homes face severe damage or destruction at these wind speeds, while even well-constructed frame homes experience substantial damage. Trees don’t just lose branches – they get uprooted entirely.

Power outages stretch from several days to weeks. Hurricane Ike in 2008 showed Texas what “extensive” really means, requiring widespread roof replacements and structural repairs across Houston.

Category 3: 111-129 mph – “Devastating Damage”

Welcome to major hurricane territory. Category 3 storms mark the point where the saffir simpson scale shifts from “extensive” to “devastating.” At these wind speeds, even well-built frame homes lose entire roof sections and suffer serious structural damage.

The building envelope fails catastrophically. This means windows blow out, doors get torn away, and suddenly your interior becomes part of the storm’s path.

Power and water outages typically last weeks because utilities need rebuilding rather than simple repairs. Hurricane Alicia in 1983 demonstrated Category 3 power to Texans, causing devastating damage across Houston.

Category 4: 130-156 mph – “Catastrophic Damage”

Category 4 hurricanes don’t just damage communities – they fundamentally change them. Well-built homes suffer severe structural damage, and affected areas become uninhabitable for weeks to months.

At these wind speeds, entire roof systems fail – not just the shingles or surface materials, but the structural members themselves. Buildings that appear intact from a distance often require complete reconstruction rather than repair.

Hurricane Harvey in 2017 brought Category 4 winds to parts of the Texas coast, creating structural damage so severe that many communities needed months of recovery.

Category 5: >=157 mph – “Catastrophic+”

Category 5 hurricanes represent nature’s ultimate stress test for human construction. These storms cause complete roof failure and potential building collapse. The damage is so comprehensive that affected areas can remain uninhabitable for months.

Only about 40 Atlantic hurricanes have reached Category 5 status since records began, making them rare but absolutely devastating when they occur.

Hurricane Andrew in 1992 remains the benchmark for Category 5 destruction, completely erasing entire neighborhoods in Florida and fundamentally changing building codes nationwide.

How Experts Use the Scale in Forecasts & Emergency Planning

When Hurricane Harvey was bearing down on Texas in 2017, meteorologists at the National Hurricane Center didn’t just announce wind speeds – they declared it a Category 4 storm. That single number immediately told everyone from emergency managers to property owners exactly what they were facing.

The saffir simpson scale serves as the universal language of hurricane preparedness. Meteorologists use it as the backbone of every advisory, forecast, and warning they issue. When they say “Category 3,” emergency managers across Texas – from Houston to Austin to San Antonio – instantly know the timeline for evacuations, the level of shelter preparations needed, and the scope of potential damage.

Emergency managers rely on the scale for critical timing decisions. Evacuation routes become dangerous or impassable roughly 7-8 hours before a Category 2 hurricane arrives, but Category 4 storms require evacuations to begin much earlier due to their larger wind fields and more destructive power. The difference between categories literally determines whether evacuation orders go out 12 hours or 36 hours before landfall.

Building codes increasingly reference hurricane categories to set construction standards. Many coastal Texas communities now require new construction to withstand specific category winds. The devastating lessons from storms like Hurricane Alicia led to building standards that reference category classifications directly – ensuring that new construction can handle at least Category 3 winds in many areas.

Insurance companies use the scale for underwriting and catastrophe modeling. They analyze decades of category data to set premiums and reserves, understanding that the exponential damage jump between categories creates vastly different claim costs. A Category 2 storm might generate thousands of repair claims, while a Category 4 in the same area could result in total loss claims requiring complete rebuilds.

Hurricane hunter aircraft measure wind speeds directly, feeding real-time data to forecasters who assign categories and issue warnings. This measured approach means that when property owners in Dallas, Fort Worth, Lubbock, Waco, or Lakeway hear a category designation, they’re getting information based on actual atmospheric conditions, not estimates.

Scientific research on hurricane wind hazards continues to refine how category classifications translate to real-world impacts, helping improve both forecasting accuracy and damage predictions for property owners.

More info about Storm Prediction Center

Beyond Wind: Surge, Rain & Tornado Risks

Here’s what catches many property owners off guard: the saffir simpson scale only measures wind speed. Storm surge, rainfall flooding, and tornado activity don’t follow the same neat category system, which can lead to nasty surprises when “weaker” storms cause more damage than their category suggests.

Hurricane Isaac in 2012 perfectly illustrates this disconnect. As a Category 1 storm, it seemed manageable based on wind speed alone. However, its slow movement and massive size generated storm surge equivalent to a Category 3 hurricane, causing extensive flooding damage that the category classification didn’t predict. Property owners who prepared for Category 1 wind damage found themselves dealing with major flood losses instead.

Tropical Storm Allison in 2001 never even reached hurricane strength but caused more flood damage across Texas than many Category 5 hurricanes. The storm dropped over 30 inches of rain in some areas, creating catastrophic flooding that had nothing to do with wind speeds. Many property owners finded that their “minor tropical storm” preparations were completely inadequate for the actual threat.

Modern forecasting addresses these limitations by issuing separate warnings for storm surge, flooding, and tornado risks. When you’re monitoring storms that might affect your Texas property, you’ll see distinct alerts for each threat – not just the hurricane category. This means paying attention to flood watches, storm surge warnings, and tornado alerts alongside the category designation.

For property owners filing insurance claims after storms, understanding these limitations becomes crucial. Your damage might come from surge or rain rather than wind, which can affect coverage and claim documentation requirements significantly.

Criticisms, Limitations & the Category 6 Debate

While the saffir simpson scale has served us well for over 50 years, it’s not perfect. Scientists and emergency managers increasingly point out that focusing only on wind speed can paint an incomplete picture of a hurricane’s true danger.

Storm size matters tremendously for property damage, but the scale doesn’t capture it. A small Category 3 hurricane might affect one county, while a large Category 2 storm can impact an entire state. For Texas property owners, this means you can’t rely solely on the category number to gauge your risk.

The scale also misses forward speed and rainfall potential. Fast-moving storms cause different damage patterns than slow crawlers. We learned this lesson painfully with Hurricane Harvey, which stalled over Texas and dumped unprecedented rainfall despite weakening significantly after landfall.

The surge problem remains one of the scale’s biggest blind spots. When the saffir simpson scale originally included storm surge estimates, meteorologists quickly realized that surge depends on ocean floor shape, coastline configuration, and storm size – not just wind speed.

Perhaps most concerning is how rainfall causes more hurricane fatalities than wind or surge combined. Yet the scale doesn’t address this at all. Tropical Storm Allison in 2001 never reached hurricane strength but caused more flood damage in Houston than many Category 5 hurricanes.

Climate change adds another wrinkle to the debate. Scientific research on climate-driven intensification shows that while we might not see more hurricanes overall, the strongest storms are becoming more intense and maintaining their strength longer.

This has sparked serious discussion about adding a Category 6 for storms exceeding 180 mph winds. Proponents argue that as storms get stronger, we need better ways to communicate extreme risk.

However, Dr. Robert Simpson himself pushed back against this idea before his death. His argument was practical: Category 5 storms already cause maximum structural damage. Whether winds are 160 mph or 200 mph, most buildings will be destroyed.

For Texas property owners, understanding these limitations is crucial for both preparation and insurance claims. Don’t let a “lower” category number fool you into thinking you’re safe from surge, flooding, or extensive damage.

Hurricane Preparedness & Insurance Tips for Texans

Living in Texas means hurricane season is a reality we all face together. Whether you’re managing a commercial property in Houston, own a home in Austin, or run a business in Dallas, Fort Worth, San Antonio, or smaller communities like Lubbock, Waco, Georgetown, Round Rock, or Lakeway, hurricanes can reach surprisingly far inland and cause significant damage.

I’ve worked hurricane claims from the Gulf Coast all the way to Central Texas, and one thing always surprises property owners: how far inland hurricane damage can extend. That Category 2 storm that hits the coast? It can still pack enough punch to cause serious roof damage in San Antonio or knock out power for weeks in Austin.

The saffir simpson scale gives you the foundation for planning, but Texas geography adds extra complexity. Coastal properties face the triple threat of wind, surge, and rain, while inland areas might dodge the surge but still get hammered by winds and flooding.

Document everything before storm season begins. Take detailed photos and videos of your property, inside and out. Create written inventories of equipment, fixtures, and valuable items. Store these records in multiple locations, including cloud storage. When you’re filing an insurance claim after a hurricane, this documentation becomes absolutely crucial.

More info about Does Homeowners Insurance Cover Hurricane Damage?

Wind mitigation improvements can make a huge difference in both damage prevention and insurance costs. Hurricane straps, impact-resistant windows, reinforced garage doors, and proper roof-to-wall connections all help your building withstand higher category winds.

Power backup planning becomes critical when you realize that Category 2+ storms typically cause outages lasting days to weeks. Generators need to be sized properly, installed safely, and tested regularly.

More info about Commercial Hurricane Damage Insurance Claim

Understanding evacuation zones matters even if you’re not right on the coast. Storm surge can travel miles inland along bayous and rivers, and evacuation routes can become impassable hours before the storm arrives.

Using the saffir simpson scale to Gauge Your Risk

The saffir simpson scale should guide your decision-making process, but it’s not the only factor to consider. Category 1-2 storms might allow you to shelter in place if your building is well-constructed and you’re not in a flood-prone area. However, Category 3+ hurricanes typically require evacuation from vulnerable locations.

Shutter and protection decisions need to match the wind speeds you’re likely to face. Hurricane shutters rated for Category 3 winds won’t protect your windows when a Category 4 storm arrives.

Insurance deductible structures often change based on hurricane categories. Many policies have separate hurricane deductibles that kick in for named storms, and these deductibles frequently increase for major hurricanes (Category 3+).

Choose your evacuation trigger point before storm season starts. Don’t wait until you’re watching weather updates every hour to decide when you’ll leave. The key is making these decisions when you’re thinking clearly, not when you’re stressed and watching storm coverage around the clock.

Frequently Asked Questions about the Saffir-Simpson Scale

Does the scale include storm surge or rainfall?

No, the current saffir simpson scale focuses exclusively on sustained wind speeds. This is actually one of the biggest misconceptions property owners have about hurricane categories. Storm surge and rainfall get their own separate warnings because they depend on completely different factors than wind speed.

Think about it this way – a small, fast-moving Category 4 hurricane might produce less storm surge than a large, slow-moving Category 2 storm. The surge depends on the storm’s size, how fast it’s moving, the shape of the coastline, and even the depth of the ocean floor. Rainfall works similarly – some storms are “dry” hurricanes with relatively little rain, while others dump incredible amounts of water regardless of their wind speed.

This is why we always tell Texas property owners to monitor multiple forecasts, not just the hurricane category. A Category 1 storm might still flood your property if it stalls over your area for days, while a Category 3 hurricane might cause mainly wind damage if it moves through quickly.

What counts as “sustained wind” when assigning a category?

Sustained winds in the saffir simpson scale are measured using a 1-minute average at 33 feet above the surface. This might sound technical, but it’s actually pretty important for understanding what the categories really mean for your property.

The 1-minute average captures the steady, persistent wind force that actually damages buildings – not the brief gusts that might be much higher but don’t last long enough to cause structural failure. It’s like the difference between someone pushing steadily on your door versus giving it a quick shove.

Here’s something interesting: other parts of the world use a 10-minute average instead of our 1-minute standard. This means the same storm might get different category ratings depending on which system you use. For Texas property owners, just remember that our system focuses on the sustained force that’s most likely to damage your roof, siding, and windows.

Why are Categories 3-5 called “major hurricanes”?

Categories 3, 4, and 5 earn the “major hurricane” designation because they cross a critical threshold for catastrophic property damage. It’s not just that they’re stronger – the jump from Category 2 to Category 3 represents a fundamental change in what the storm can do to well-built structures.

At Category 3 winds (111+ mph), even properly constructed homes start losing roofs and suffering structural damage. Below that threshold, you’re mainly looking at surface damage – shingles, siding, gutters, and tree branches. Once you hit major hurricane status, the storm starts attacking the bones of the building itself.

From an insurance perspective, major hurricanes often trigger different deductible structures and coverage provisions. Many Texas policies have separate “hurricane deductibles” that only apply to major hurricanes, reflecting the exponentially higher damage costs these storms typically generate.

The designation also helps emergency managers communicate the seriousness of the threat. When forecasters say “major hurricane,” they’re telling you this isn’t just a strong storm – it’s a storm that can fundamentally change communities and require months of recovery time.

Conclusion

Understanding the saffir simpson scale gives you a crucial foundation for hurricane preparedness, but remember – it’s just the starting point of your storm planning journey. Throughout our exploration of Categories 1 through 5, we’ve seen how Texas hurricanes like Harvey, Ike, and Alicia taught us that wind speed alone doesn’t tell the whole story.

The scale’s beauty lies in its simplicity – those five categories instantly communicate wind damage potential to millions of people. But as any Texan who’s weathered a hurricane knows, the real threat often comes from what the scale doesn’t measure: storm surge that floods entire neighborhoods, rainfall that turns streets into rivers, and the unique way each storm interacts with our local geography.

Don’t let a “lower” category number fool you into thinking you’re safe. We’ve handled insurance claims from Category 1 storms that caused hundreds of thousands in damage and Category 2 hurricanes that left communities rebuilding for months.

Throughout hurricane season, stay alert and monitor National Hurricane Center updates religiously. Weather can change rapidly, and that Category 2 storm in the morning forecast might be a Category 4 by evening. When evacuation orders come – regardless of category – act promptly.

Document everything before and after storms hit. Take photos, create inventories, and keep detailed records. When dealing with hurricane damage claims, this documentation becomes your lifeline for proving losses and securing proper settlements.

At Insurance Claim Recovery Support LLC, we’ve guided property owners across Texas – from the Gulf Coast to Austin, Dallas to San Antonio, Houston to Lubbock, and everywhere in between – through the complex world of hurricane insurance claims. Our experience shows that while the saffir simpson scale helps predict the storm, expert claim handling determines your recovery success.

Whether you’re facing Category 1 roof repairs or Category 5 total reconstruction, having experienced public adjusters who understand both hurricane science and insurance complexities makes all the difference. We ensure you receive every dollar you deserve, turning the chaos of storm damage into a manageable path toward full recovery.

The scale helps us prepare for what’s coming. We help you recover from what it leaves behind.